Will China dominate the construction equipment market?

Are Eastern manufacturers primed to be the new global superpowers of the industry? Global chief technology officer at Pullmann Global, Alan Berger shares his insights below:

Only five years ago, the construction equipment sector was suffering a significant drop in demand, with sales bottoming out at around 700,000 machines per year. In subsequent years, we experienced rapid growth and by 2018 equipment sales had increased by over 50% to approximately 1.14 million machines.

What has driven such growth?

“The industry sometimes forgets that it is cyclical, with a relatively consistent long-term growth rate that is related to global GDP and population growth. So, on the one-hand the recent growth is just the recovery part of the most recent downward cycle. Looking a bit deeper using data from Off-Highway Research, we see that China, with India playing a supporting role, has driven most of this growth.”

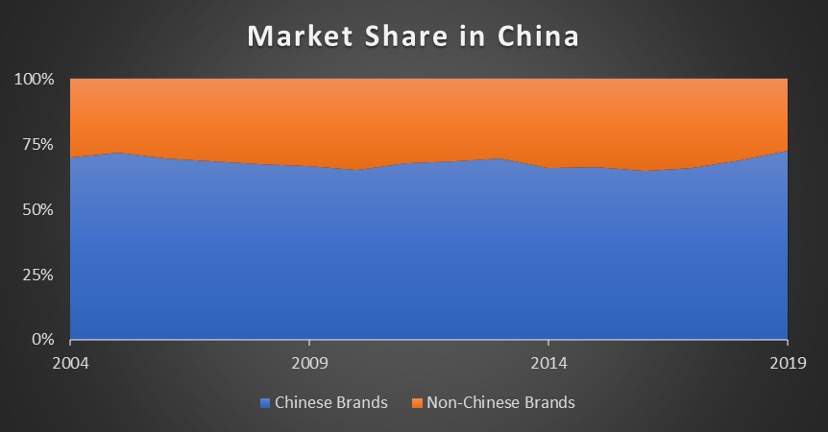

Who are the winners of this expansion in China?

“This is where it gets interesting. While the non-Chinese brands have invested heavily in China for many years, the data shows that over the past 15 years that share of all non-Chinese players in China is essentially flat.

“So, despite all that focus and huge investment what is the result? No share growth.”

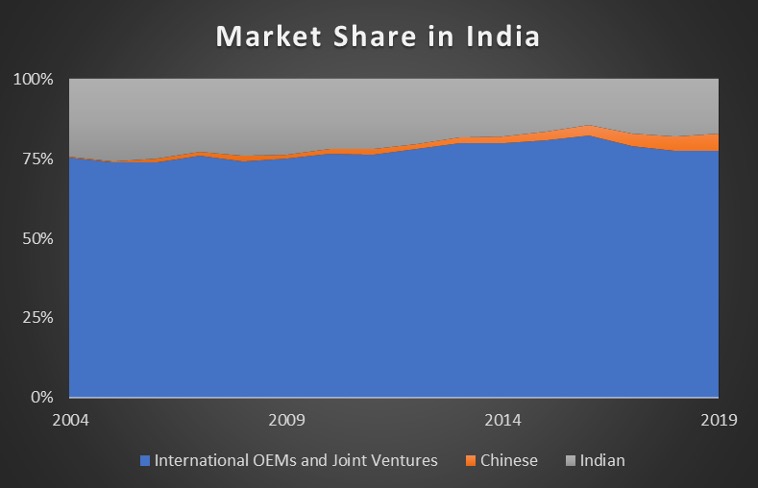

What’s the story in India?

“India is a bit different, where the traditional global players have held their share even as they have integrated their early joint ventures, while the domestic players have been losing to the Chinese in recent years.”

Is there a market for premium products in these markets?

“The evidence is that there is a market, but it is limited. Clearly value products are taking share in India even as the market matures. If we look deeper in China, we can see that when we remove the dominant effect of wheel loaders, the non-Chinese share of all other products (which is then dominated by excavators) is dropping – fast.

“This suggests to me that as the Chinese products mature to an acceptable level, the market is moving towards these somewhat lower spec, but perfectly adequate products. It also speaks to the process that has been going on globally for some time, where all construction equipment products are commoditizing and the ace card that the Chinese players enjoy is their superior local distribution.”

Electrification is topical within both on/ off-highway applications as the sector explores alternative propulsion options for the future. Considering the global market, who do you feel will emerge as the leader?

“We tend to overly focus on battery electric or electric hybrids when we talk about this. But there are many other alternatives, each with their own pros and cons, and in some special cases even better climate change implications than electrification. Sticking to electrification, today we see big investment from many of the largest OEMs, with a focus on the European market. These would be the usual players you would expect to have the resources and ability to make such a significant technology change. But we just spoke about commoditization and the local success that the Chinese are having with their own products.

“If we look across to the automotive sector where most vehicle technologies start life, we see that China as a country has put a huge focus on electrification and (arguably) has the technology lead overall, and without question, on batteries. I also believe that the most successful electrification efforts are not going to be just replacing the diesel engine with batteries and electric motors, but re-architecting machines to take full advantage of the different characteristics that electrification brings.

“Taken together, this means that some of the traditional OEM strengths are not important and could even be a hinderance. I think it is a distinct possibility that the Chinese OEMs will win the electrification race.”

Considering the current COVID 19 situation, how do you see this impacting the industries investment in technology and product development? Do you foresee a slowdown in any particular areas?

“Clearly, we see the industry forecasts for 2020 showing a significant overall market slowdown. This always causes the OEMs to prioritize their R&D investments, trying to maintain a balance of long-term R&D while making sure the most beneficial shorter-term projects proceed.

“Given the challenge of maintaining the current portfolio, doing the typical incremental progression of efficiency, productivity, and comfort – and at the same time wrestling with the megatrends of autonomy, alternative propulsion and connectivity, something will have to give.

“While all are important, I see electrification as critical, for at least small machines that operated in cities in Europe, where diesel restrictions are already in place. Connectivity investment will also continue, as it offers short-term value and clear customer demand. This leaves autonomy as the most likely to have the brakes applied, unless some OEMs make the bold move of slowing down their development of their existing portfolio to protect R&D spending.”

Alan Berger, Global chief technology officer and Founding Partner at Pullmann Global has worked in the vehicle industry for over 25 years. He has lead product development for Volvo Construction Equipment, and was the Chief Technology Officer at CNH Industrial, focusing on leadership, product development efficiency and the digital and electrification transformation.