The Ten Trillion Bet on Intelligent Infrastructure

The world’s roads, railways, ports, airports, power grids and utilities are no longer being valued as lumps of concrete, steel, pipework, cables and regulated cash flow. Increasingly, they are being repriced as operating systems for trade, mobility, energy security, urban life and industrial competitiveness. That shift is pulling infrastructure out of the engineering pages and into the macro pages.

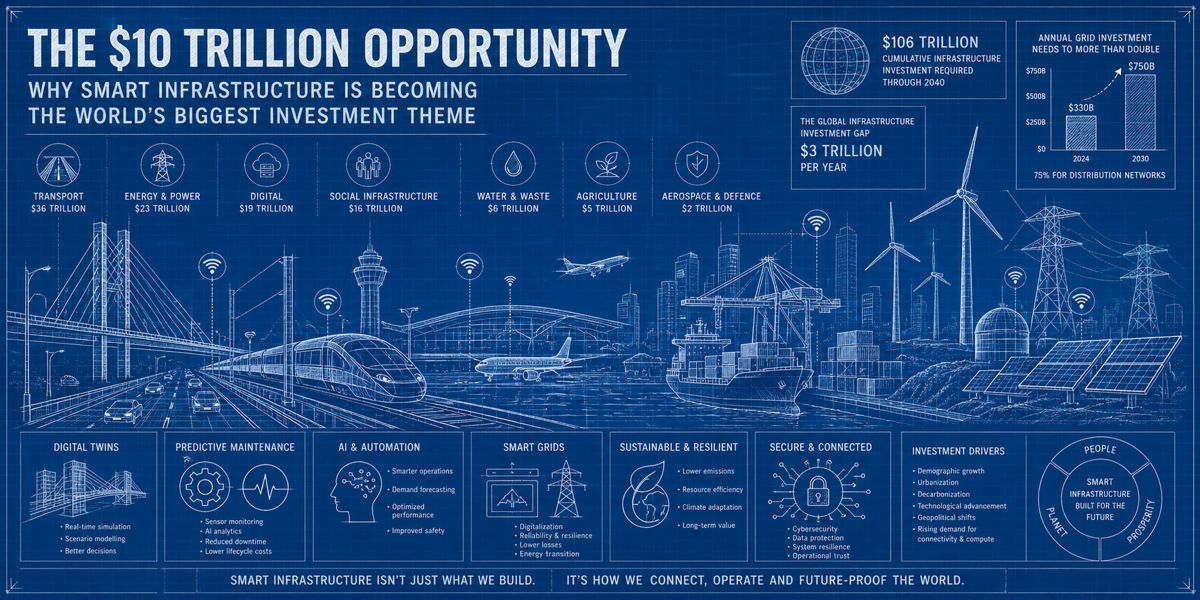

A conservative aggregation of credible forecasts already pushes the opportunity comfortably beyond US$10 trillion over the coming decades. McKinsey & Company now puts the figure at US$106 trillion of cumulative infrastructure investment required through 2040, spread across seven verticals: transport at US$36 trillion, energy and power at US$23 trillion, digital at US$19 trillion, social infrastructure at US$16 trillion, waste and water at US$6 trillion, agriculture at US$5 trillion, and aerospace and defence at US$2 trillion. The Global Infrastructure Hub puts the global infrastructure investment gap at around US$3 trillion a year. The International Energy Agency says annual grid investment alone needs to more than double, from around US$330 billion to roughly US$750 billion by 2030, with three-quarters of that flowing into distribution networks.

That is before counting the software, sensor, data and automation layers now attaching themselves to every serious asset plan. Of equal importance is where the money is going within those totals. McKinsey estimates nearly US$7 trillion in data centre investment alone may be needed through 2030 to keep pace with compute demand, while Société Générale’s infrastructure team puts the four-year data centre figure at US$7 trillion to US$8 trillion. That is an extraordinary acceleration, and it is already reshaping where infrastructure capital is forming.

As Alastair Green, McKinsey’s senior partner who leads the firm’s infrastructure work, told an industry summit in Los Angeles in September 2025, “The definition of infrastructure is changing,” noting that the term now spans more than 100 asset types across seven verticals, around 30% of which are relatively new.

The crucial point is that smart infrastructure is not a niche technology story bolted onto traditional public works. It is becoming the way infrastructure gets financed, built, operated and defended. Transport networks, grids, water systems and ports are all developing a digital exoskeleton of sensors, twins and analytics that increasingly determine how the underlying asset is valued. The International Energy Agency argues digital solutions can extend asset life and defer an estimated US$1.8 trillion of grid investment globally to 2050. UN Trade and Development argues that digitalisation through AI, automation and blockchain is now central to reducing port delays and improving cargo visibility.

This isn’t simply about building more assets. It is about upgrading the intelligence, resilience and revenue quality of the assets already there, and of the ones that still have to be built.

Briefing

- Global infrastructure demand is already measured in tens of trillions, and the digital layer inside that spend is growing faster than the rest, with data centres and energy accounting for a major share of recent infrastructure deal value.

- Roads, rail, ports, airports, grids and water systems are moving from reactive maintenance towards data-led operations, predictive asset management and digital twin platforms.

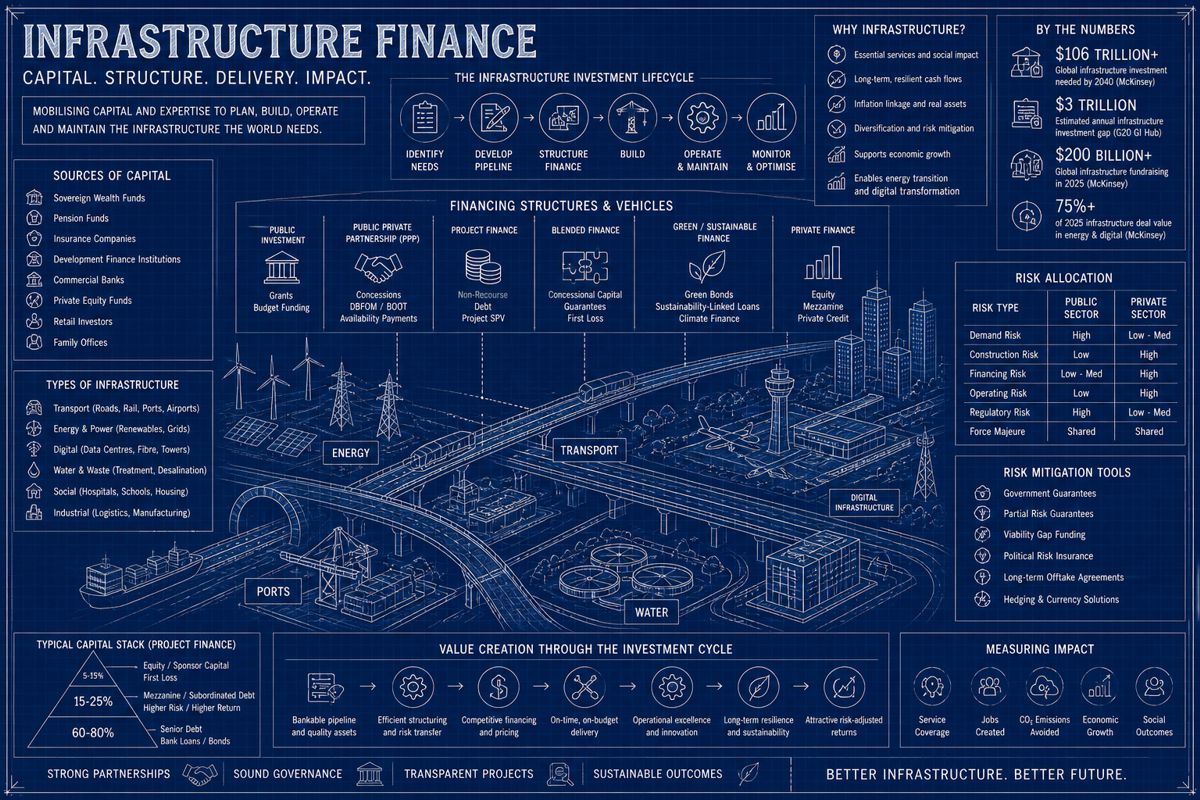

- Private capital is interested, but it still needs bankable pipelines, risk-sharing structures, regulatory clarity and interoperable data.

- Sovereign wealth funds, blended finance vehicles and hybrid PPPs are starting to matter more because public balance sheets are under pressure.

- Emerging economies may have a chance to leapfrog older networks by embedding digital capability at the build stage rather than retrofitting it later, although cybersecurity and skills shortages are becoming central risks.

Infrastructure Has Become A Macro Asset Class

For years, infrastructure investing was sold on a fairly familiar pitch: stable cash flow, inflation linkage, monopoly-like characteristics and useful diversification away from traditional equities. That argument still holds, but it is no longer the whole story. The newer and more forceful argument is macroeconomic. Global supply chains are fragmenting, electricity demand is climbing, defence and industrial policy are back in fashion, urban capacity is tightening and AI is intensifying demand for power, fibre and data-centre ecosystems.

As McKinsey’s senior partners Adrian Kwok, Alastair Green and Connor Mangan put it in their 2026 outlook, the world now sits at “an emerging intersection of systems and facilities across verticals, including data centers, charging stations, fiber-optic networks, and more,” calling for a “fundamental mindset shift” among governments, investors and industry operators about how to fund, build, use and maintain infrastructure.

That widening brief is showing up in portfolio preferences. McKinsey reports that global infrastructure fundraising hit nearly US$200 billion in 2025, surpassing the previous high of US$180 billion in 2022. Its late-2025 LP survey found infrastructure delivered the largest expected net shift in target allocations over a three-year horizon. The World Economic Forum notes that the value of dedicated infrastructure assets held by private-capital firms has tripled since 2016 to roughly US$1.5 trillion, with 46% of private market investors planning to increase their infrastructure allocations.

Investors are, in effect, paying up for assets that can absorb technology, not just endure depreciation. That is a very different mindset from the old concession-era view of infrastructure as a passive income sleeve. The winners are not simply the assets with the longest concession periods or most predictable tariff structures. Increasingly, they are the assets with the clearest route to higher utilisation, better data, lower failure rates and stronger resilience.

The geographic concentration of need is striking. McKinsey projects Asia will require around US$70 trillion of the global $106 trillion total, with the Americas at US$16 trillion, Europe at US$13 trillion, Africa at US$5 trillion and Oceania at US$2 trillion. As Massimiliano Battisti, Société Générale’s global head of infrastructure, telecom, media and technology, told the bank’s clients in late 2025: “There is room for everyone.” He also added a useful warning: even if the current AI-driven boom slows and individual players need restructuring: “all of the assets being built today will be required by someone in some form.”

That distinction matters. Even where market froth exists around AI, data centres or digital infrastructure, the underlying assets are not purely speculative. Power connections, fibre routes, cooling systems, grid upgrades and compute campuses may change ownership or tenant profile, but the physical demand for digital capacity is unlikely to disappear.

Public Balance Sheets Cannot Do It Alone

The public sector is still central, but fiscal reality is getting in the way. The OECD has warned that higher and more expensive sovereign debt risks constraining the capacity to finance future investment needs, with sovereign bond issuance reaching new highs and outstanding debt continuing to rise. That does not mean governments will stop spending on infrastructure. It means they will be choosier, slower and more interested in structures that crowd in outside money.

In low- and middle-income countries, the World Bank reported that private participation in infrastructure investment reached US$100.7 billion in 2024, the first time it cleared the US$100 billion mark since the pandemic. Useful, yes. Enough to close a US$3 trillion annual gap, plainly not.

The mismatch between need and available capital is still striking. Jamie Torres-Springer, president of the New York City MTA’s Construction & Development unit, captured the tone neatly at the McKinsey infrastructure summit in Los Angeles, telling delegates: “We are desperate for a diversification of funding.”

That sentence could have come from almost any transport authority, utility regulator, port operator or urban government dealing with ageing assets and rising expectations. Once an operator starts promising not just a road or a wire but a data-rich, resilient, cyber-secure operating platform, capital structures have to become more sophisticated too.

The OECD’s Africa Development Dynamics 2025 report is instructive. Between 2013 and 2023, official development finance mobilised almost US$57 billion of private capital for African infrastructure, but 45% of that came in the form of guarantees. Just five countries, Ethiopia, Egypt, Nigeria, Kenya and Côte d’Ivoire, captured 52% of the total. Capital travels to project pipelines that are bankable and to institutions that can manage them. Smart infrastructure makes that challenge more urgent, not less.

The lesson for policymakers is blunt. Digital ambition is not enough. Investors need procurement certainty, credible demand models, realistic tariff structures, currency-risk mitigation, long-term maintenance obligations and public counterparties that can execute. Without those foundations, smart infrastructure remains a slide deck rather than a market.

Transport Networks Are Becoming Data Networks

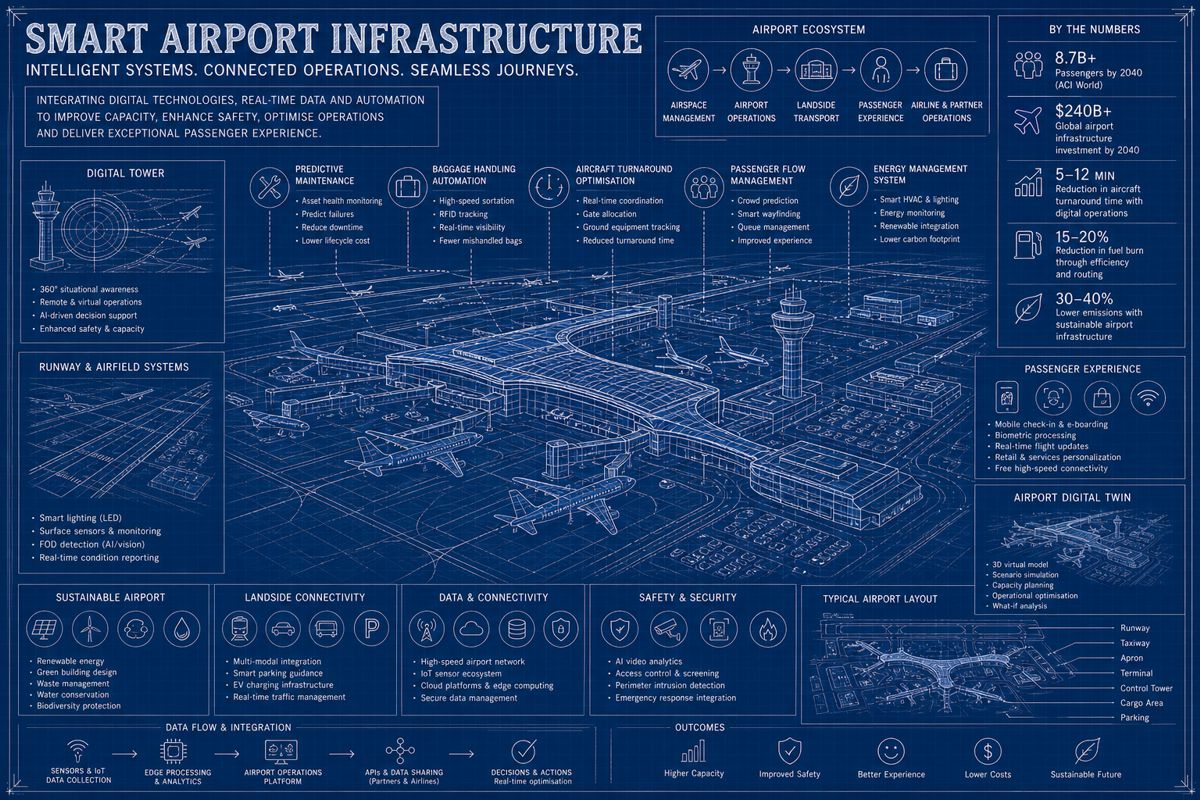

Transport is where the shift becomes easiest to see. McKinsey’s 2025 work projects transport and logistics will absorb the largest share of global infrastructure spending through 2040 at US$36 trillion. Yet the commercial story is not merely the quantity of asphalt, track, runway or terminal floor area. It is the intelligence layer that governs utilisation.

The Airports Council International says passenger demand is set to rise sharply in the decades ahead while airport finances remain strained. That creates a premium for digital systems that squeeze more throughput and reliability from the same footprint. Expanding a terminal, adding a runway or building a new port basin will always matter. But squeezing more capacity from existing assets is often faster, cheaper and politically easier.

The numbers being recorded by leading operators are now serious enough to move balance sheets. Bentley Systems documents that Sydney Airport saved more than 12,000 hours per year by managing assets with a digital twin. Guangzhou Baiyun International used 4D modelling to lift construction efficiency by 25%. U.S. engineering firm Benesch reduced manual fieldwork by 75% using AI-powered crack detection.

Research published in International Airport Review in late 2025 indicates that real-time tracking of ground equipment using digital-twin-fed monitoring of fuel trucks, catering vehicles and baggage handling has reduced aircraft turn times by five to twelve minutes. Analysis attributed to Kelly Watt of DFW Airport in that research suggests that one or two additional rotations per gate per day at a major hub could add US$15 million to US$25 million in annual aeronautical revenue.

Stack that against the FY2025 terminal rental rate of roughly US$337 per square foot at DFW and the implication is clear: gates are revenue assets, and digital twins can shift the unit economics of those assets in a way that physical expansion alone cannot.

At sea, the Port of Singapore launched its Maritime Digital Twin in March 2025, joining a small group of global ports operating mature, integrated twin systems. Qingdao in China has gone further, deploying its Ark TaaS, or “Trade as a Service”, platform in beta from early 2025, using big data and large-scale AI models to optimise route planning and delivery.

Ke Wang, a port digitalisation specialist quoted in the Port of Barcelona’s PierNext analysis, summed up the operational benefit: “Qingdao aims to achieve smoother coordination between terminals, improve cargo visibility, and reduce downtime, which will contribute to more sustainable and competitive port operations.”

For investors, the read-across to maritime concession revenue, dwell-time clauses and supply-chain insurance pricing is more direct than it would have been even three years ago.

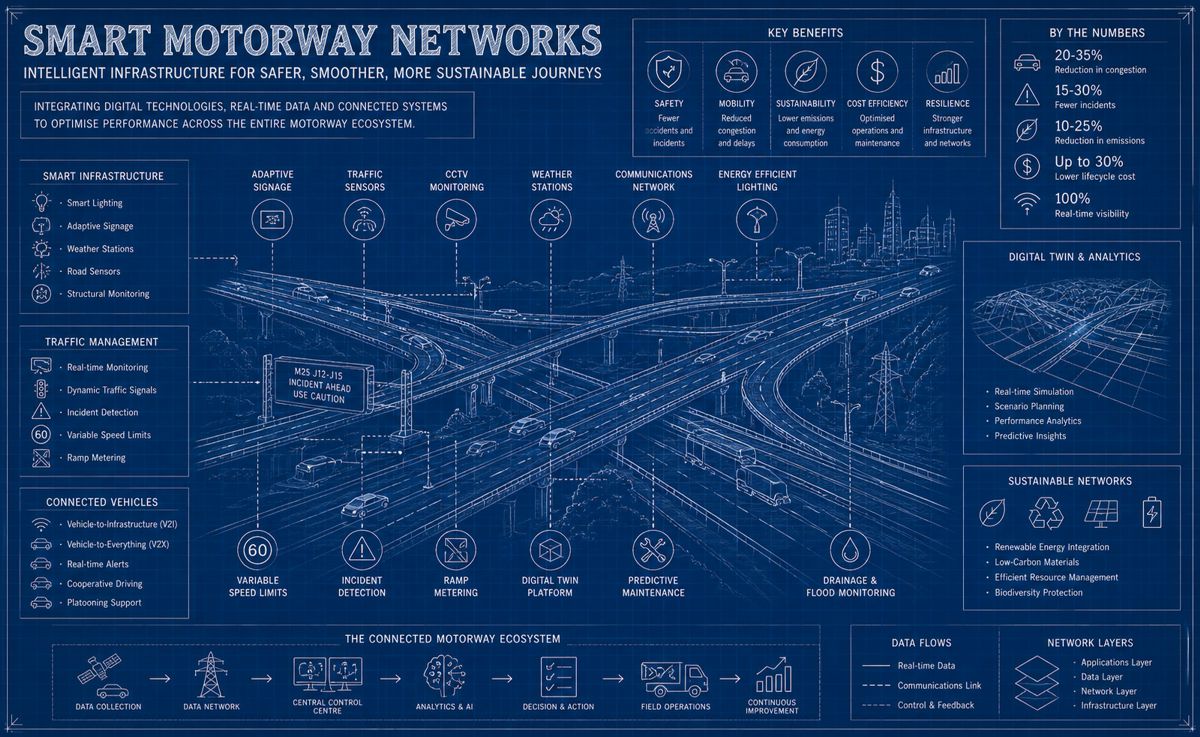

The road story is moving the same way. The Global Infrastructure Hub’s use-case library now treats dynamic traffic management, intelligent tolling, smart containers and sensor-led traffic operations as mainstream extensions of transport infrastructure rather than science projects. A World Bank-supported smart mobility programme in Brazil focused on smart traffic lights, bus-priority systems and control platforms designed to improve congestion, safety and operations.

None of that sounds glamorous, and that is partly the point. Infrastructure technology rarely needs a moon-shot narrative to create value. It needs a measurable effect on throughput, maintenance burden, incident detection, staffing efficiency and user experience. Once those benefits are priced into PPPs, concessions or regulated asset plans, the digital layer stops looking like discretionary kit and starts looking like core infrastructure expenditure.

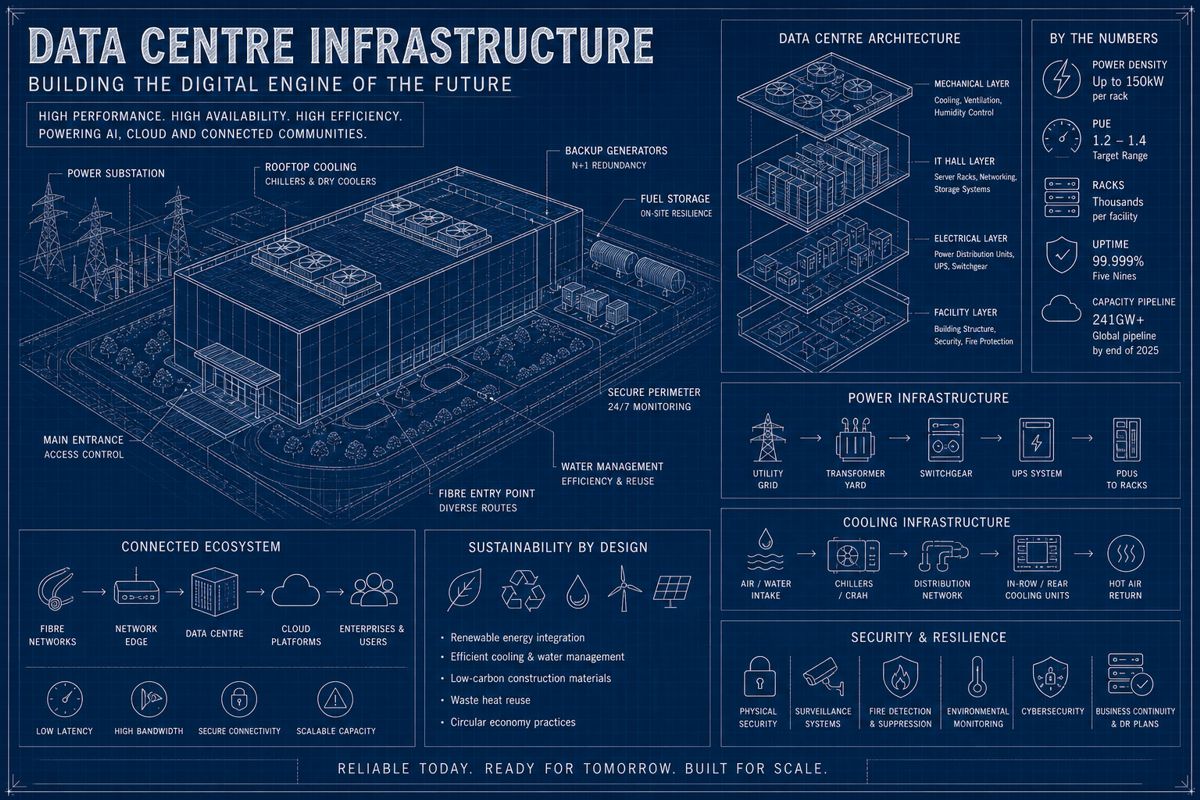

Data Centres Are Becoming The New Flagship Infrastructure Asset

If smart infrastructure has a poster child in 2026, it is the data centre. The category has moved, in less than three years, from a fringe interest of specialist real estate funds to one of the largest concentrations of infrastructure capital in the world.

McKinsey’s 2025 analysis estimates that companies across the compute power value chain will need to invest $5.2 trillion in data centres by 2030 to meet AI-related demand alone, with 156 gigawatts of AI-related capacity required by the end of the decade and 125 incremental gigawatts to be added between 2025 and 2030. Société Générale’s bankers put the four-year figure at US$7 trillion to US$8 trillion. McKinsey’s deal data shows energy and digital infrastructure together captured roughly three-quarters of all 2025 infrastructure deal value.

Whatever number is chosen, the directional message is the same. Data centres are now where the marginal infrastructure dollar is going.

The scale of individual projects is hard to grasp without examples. CBRE reports primary U.S. market supply rose 36% year-on-year to 9,432 MW in H2 2025, with record net absorption of nearly 2,500 MW. Northern Virginia alone absorbed 1,102 MW in 2025, while gigawatt sites in Ohio, Michigan, Texas and Pennsylvania are being assembled with the kind of land, water and power packages historically associated with petrochemical complexes.

By the end of 2025, over 241 GW of data centre capacity sat in the global development pipeline, a 159% increase in twelve months. A single hyperscale campus can now draw as much as 11 gigawatts of power, more than 10% of the entire Texas grid’s record peak. Bloom Energy projects U.S. data centre IT load doubling from roughly 80 GW in 2025 to 150 GW by 2028, with nearly one-third of campuses expected to exceed a gigawatt by 2035.

The reason this matters for the broader infrastructure thesis is that data centres are effectively forcing a rebuild of the assets around them. Power availability has overtaken capital, land and connectivity as the primary constraint on growth. In Northern Virginia, which hosts more than 70% of global internet traffic, wait times for new power connections can exceed five years. Major U.S. markets are seeing three to seven-year delays for transmission upgrades. Lead times for transformers and switchgear have stretched twelve to eighteen months beyond historical norms.

Hyperscalers have responded by becoming, in effect, energy infrastructure developers themselves. They are signing direct PPAs with renewables developers, contracting nuclear restarts and small modular reactor capacity, building behind-the-meter gas generation, and committing more than 50 GW of clean energy to date.

As a hyperscaler energy executive quoted in Bloom Energy’s 2025 industry survey put it: “We’re seeing a geographic shift as certain regions become more power-friendly and therefore more attractive for data center construction.” Texas is on track to become the largest U.S. market by 2028 with over 40 GW of capacity, displacing Virginia precisely because the grid headroom is bigger.

The financial architecture has changed in lockstep. Transactions for individual greenfield campuses now regularly exceed $1 billion. Landmark deals such as the signed but not yet closed US$40 billion acquisition of Aligned Data Centers by the Artificial Intelligence Infrastructure Partnership, involving BlackRock’s GIP, MGX and Microsoft, define a new tier of asset.

Alphabet, Amazon, Microsoft and Meta alone are projected to spend more than $350 billion on data centres in 2025 and US$400 billion in 2026, with hyperscaler capex forecast to exceed US$600 billion in 2026, roughly 75% of it tied to AI infrastructure. DigitalBridge’s flagship fund series targets 15% to 20% gross IRR across the digital infrastructure stack, with closed-end infrastructure funds typically returning 12% to 18% gross IRR over a 10 to 12-year fund life.

These are growth-equity returns dressed in infrastructure clothes, which helps explain why sovereign wealth, pension and private credit capital have all converged on the category.

But this flagship asset comes wrapped in flagship-sized risks. Power constraints are reshaping where, when and whether projects move forward. Anirban Basu, chief economist of Associated Builders and Contractors, warned ENR in early 2026 that “if these projects don’t deliver a return on investment relatively quickly, you could see a sharp pullback. The higher the construction costs, the more debt is required to finance them.”

Public-market exit channels remain shallow relative to fund holdings. Hyperscaler tenant concentration creates a meaningful credit-risk overhang. National security reviews in the U.S., U.K. and EU are tightening. The technology stack underneath, from chip generations to cooling regimes and rack densities now reaching 80 to 150 kW for AI workloads versus 10 to 15 kW historically, is moving fast enough that obsolescence is a live concern.

Data centres may be the new flagship, but they are also the most leveraged bet within the smart-infrastructure trade. The investors and operators who win here will be the ones who treat them less as real estate and more as integrated power-and-compute platforms with industrial-scale operating risk.

Utilities Are Turning Into Intelligent Platforms

Utilities may be the clearest case of all, because the old model is under such obvious pressure. The IEA says annual grid investment must rise from around $330 billion per year to about US$750 billion by 2030, with roughly three-quarters of that spend directed towards distribution networks.

As IEA executive director Fatih Birol put it: “Power grids are among the unsung heroes of the energy transition, but they need massive investment… By digitalising our grids, our power systems become more reliable and secure, and our utilities can better manage the balance of electricity supply and demand.”

The agency also notes that grid technical losses already account for roughly 1 gigaton of CO₂ emissions annually, twice the emissions of all cars in Europe. It estimates that without an improvement in supply security enabled by digital technologies, lost-revenue costs in emerging markets could reach US$1.3 trillion through 2030.

The funding response is starting to match the rhetoric. The European Commission’s “Digitalisation of the energy system” action plan anticipates around €584 billion of grid investment by 2030, of which €170 billion is earmarked specifically for digitalisation. China has committed roughly US$442 billion for grid modernisation across 2021 to 2025. Japan announced a US$155 billion smart-power programme in 2022, while India’s Revamped Distribution Sector Scheme carries roughly INR 3.03 trillion, about US$38 billion, to support distribution companies and improve infrastructure.

These are not pilots. They are explicit national commitments to rebuilding the most under-invested layer of the electricity system while adding intelligence to it.

The same logic is creeping across water networks. The World Bank’s Digital Water programme is explicitly built around smart metering, predictive maintenance, active leak detection, remote sensing, GIS, data integration and cybersecurity for utilities contending with ageing systems, drought, climate shocks and urban growth.

The empirical case is becoming hard to ignore. Singapore’s PUB has rolled smart water meters through residential customers nationwide, with documented savings of 5% to 17% on household consumption and overconsumption alerts dropping from 9% to 3% of customers. Thames Water in the UK has been installing smart meters since 2013 in its highest-leakage zones, aiming to provide all 9 million customers with their own meter by 2030, and reported a year-on-year leakage reduction of 13.8% in 2019/20.

Microsoft’s collaboration with FIDO from 2023 deployed an acoustic AI tool, running OpenAI’s GPT-4 on Azure, to detect leaks in Thames Water’s London network. Results have been encouraging enough that the model is being replicated across other utilities globally.

Taken together with the IEA’s observation that global smart-power meters exceeded one billion in 2022 and connected devices are heading into the tens of billions, the picture is clear enough. Utilities are being rebuilt as intelligent platforms that happen to own pipes, substations, transformers and pumping stations, not the other way round.

Sensors And Predictive Maintenance Are Rewriting The Maths

If the headline capex is what draws attention, operational economics are what make the theme genuinely investable. Predictive maintenance has become the most persuasive example because it attacks one of infrastructure’s oldest weaknesses: the habit of waiting too long to intervene, then paying too much when something finally breaks.

The Global Infrastructure Hub describes predictive maintenance as the use of sensors, communications systems and machine-learning analytics to detect deterioration, optimise maintenance schedules and extend asset life across critical assets such as pipes, pumps and motors. McKinsey’s 2025 analysis of digital twins argues that public-sector capital and operational efficiency could improve by 20% to 30% when infrastructure decisions are modelled, stress-tested and managed through digital replicas.

Those are not trivial gains in sectors where margins are modest, capital lives are long and service failures carry political consequences.

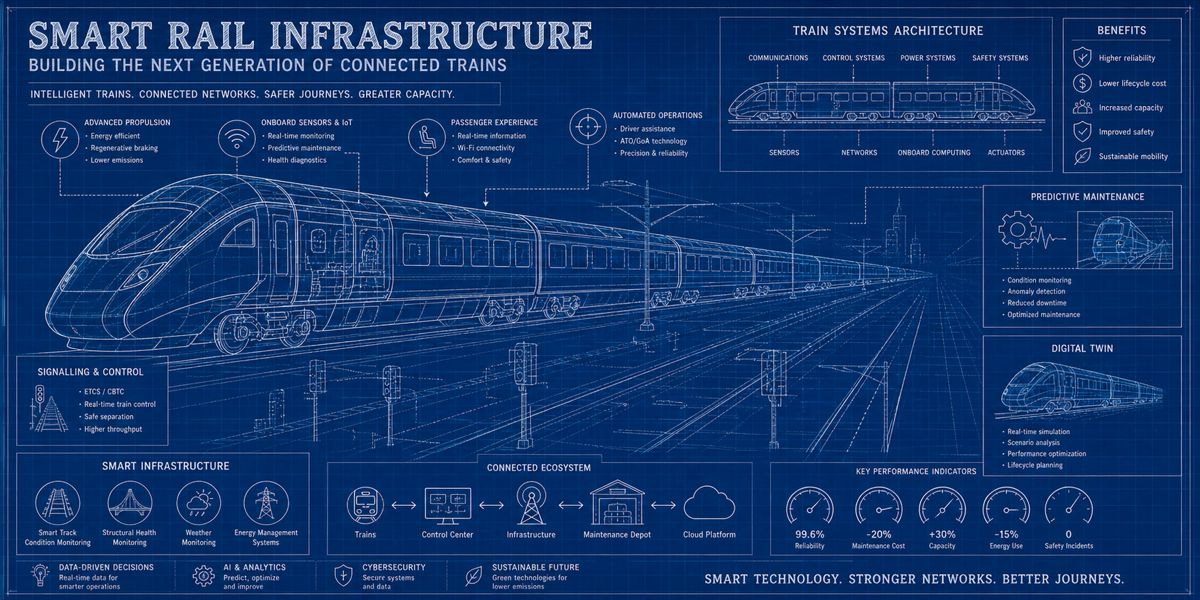

The rail sector is already speaking this language in a matter-of-fact way. A report from the International Union of Railways says predictive maintenance for rail infrastructure can typically cut unplanned downtime by 15% to 25%, lower maintenance costs by 15% to 30%, double failure-capture capacity and reduce delays per service by around 20%.

SNCF, France’s national rail operator, has gone further than most. In an interview with the company’s communications team, Cyril Verdun, SNCF’s Director of Maintenance Engineering for Rolling Stock, explained that the operator now analyses more than 8,000 variables per train, with 2,000 in real time, monitoring over 1,100 trains simultaneously. His most striking claim: “we can eliminate routine preventive maintenance — inspecting trains, checking a level, a value, a condition — which probably accounts for around 90% of maintenance work.”

The case studies stack up across the sector. According to an October 2025 industry analysis, Deutsche Bahn now ingests over 28 terabytes of data monthly from 3,500 sensors across its fleet, with predictive systems identifying 90% of component failures before they impact service and improving punctuality by 30%.

Network Rail’s digital platform, which integrates weather, vibration and maintenance data, has produced a 10% reduction in track incidents and 20% cost savings across preventive tasks. India’s SMART programme, integrating IoT sensors and analytics across the world’s fourth-largest rail network, has reduced annual breakdowns by 28%, lifted mean time between failures by 22% and cut maintenance cost per kilometre by 18%.

Where ROI calculations have been published, payback windows of 6 to 12 months are common for mid-sized agencies, with a single avoided derailment offsetting platform costs many times over.

AI Is Moving Maintenance From Guesswork To Probabilities

Roads, bridges and airports are travelling in the same direction. The Global Infrastructure Hub’s Italian bridge-maintenance case study describes how sensors, robotic systems, dehumidification controls and a dedicated monitoring database can support continuous supervision and maintenance planning on a motorway bridge. The value proposition is blunt: lower corrosion risk, lower energy use, fewer dangerous manual interventions and twenty-four-hour visibility of structural condition.

A development bank digital twin road-construction case cited by the Asian Development Bank reported a 10% cost reduction, equivalent to US$3.2 million, as well as lower emissions and improved safety outcomes after the design was reworked with digital analysis. That sort of gain matters because it arrives before the first repair crew is even dispatched. Smart infrastructure, at its best, starts reducing life-cycle cost before the asset enters service.

The market is voting on these results. The global digital twin market for infrastructure was worth US$3.8 billion in 2022, and MarketsandMarkets projects a compound annual growth rate of 60.6% to US$48.2 billion by 2026. That is among the steepest curves of any infrastructure technology category.

Indira Gandhi International Airport in Delhi uses AI-powered predictive models alongside three runways equipped with CAT-III Instrument Landing Systems to enable safe landings in low-visibility conditions, blending physical landing aids with software-driven decision support. London Luton has launched a partnership with the University of Bedfordshire to function as a live innovation testbed for AI-driven airport solutions.

ACI Europe’s innovation material consistently emphasises digital twins and predictive analytics as tools for real-time monitoring and proactive decision-making. Seen from a finance-led perspective, AI and sensor stacks do not merely support infrastructure. They increase the effective yield on existing infrastructure, which is another reason the asset class is starting to look more like growth infrastructure than static utility income.

Sovereign Wealth Funds And PPPs Are Learning New Tricks

The financing side of the story is changing because the investor base is changing. The International Forum of Sovereign Wealth Funds reports that sovereign wealth funds invested US$9.4 billion across 53 digital-theme deals in 2024, with US$5.4 billion channelled into digital infrastructure such as data centres and telecoms, up 54% from the previous year.

By 2025, that trickle had become a torrent. In November 2025, the Qatar Investment Authority anchored Blue Owl’s $3 billion data centre platform with a US$1 billion equity commitment. That formed part of a wider pledge by QIA’s CEO Mohammed Al-Sowaidi to deploy US$500 billion in U.S. investments, particularly in AI and data centres, over the coming decade.

The pattern is global. Singapore’s GIC partnered with Equinix on hyperscale joint ventures across multiple markets and acquired a 25% stake in a new Spanish fibre platform alongside MasOrange and Vodafone Spain for €1.4 billion. Abu Dhabi Investment Authority, with roughly $993 billion of assets under management, is building large-scale data centre development with Brookfield Asset Management.

MGX, backed by Mubadala, committed US$1.5 billion to OpenAI in early 2025 and is part of the Artificial Intelligence Infrastructure Partnership alongside BlackRock’s Global Infrastructure Partners and Microsoft, the consortium behind the signed but not yet closed $40 billion acquisition of Aligned Data Centers. Saudi Arabia’s PIF, with around US$700 billion of assets, has been deploying capital into digital infrastructure both at home in hyperscale campuses in Riyadh and KAEC and internationally.

That feeds directly into the evolution of PPP models. The World Bank’s PPP guidance notes that availability-based contracts allow governments to retain demand risk while paying private partners for asset availability and performance, a structure well suited to assets where reliability matters more than volatile traffic volumes or short-term user demand.

The Bank also now promotes hybrid PPPs that combine concessional support with private expertise and capital, explicitly to keep costs down and improve bankability. The detail from blended-finance work is worth noting too: according to a 2025 World Bank blog, guarantees can significantly increase commercial participation, with deals using guarantees seeing 80% private debt participation versus 42% where guarantees are absent.

Once smart infrastructure becomes a performance promise rather than a simple build promise, those contractual and credit-enhancement tools become much more important.

There is, however, a structural caution worth flagging. Dorina Yessios, partner and co-head of energy, infrastructure and natural resources at A&O Shearman, told ION Analytics in late 2025 that the investor base now spans Israeli, Australian and Spanish platforms developing alongside U.S. firms: “New entrants recognize that they need to put together the different pieces of the puzzle, and they’re coming from all around the globe.”

But she added that capital formation faces real constraints, with debt supply running well ahead of equity demand. Wendell Wilcoxen of the same firm noted that the lack of a “deep, liquid public market creates a monetization squeeze that will likely dominate 2026.” Capital is interested. It is not unconditional.

Emerging Markets May Build Smarter First Time

This is where the story starts to get especially interesting for investors with patience and nerve. Much of the public debate assumes advanced economies will lead because they have deeper capital markets and stronger institutional capacity. Yet plenty of evidence points the other way in specific subsectors.

The African Development Bank has long argued that Africa’s infrastructure deficit is not only a drag on growth but also a chance to leapfrog into more efficient technologies. Its own estimates put the continent’s infrastructure needs at US$130 billion to US$170 billion a year, with a large financing gap still to fill.

The Rocky Mountain Institute framed the situation bluntly in early 2026: “In 2025, most traditional utilities in Africa are manually operating analogue electricity systems, with limited knowledge of who their customers are and where the losses occur.” That is a problem and a leapfrog opportunity at the same time. The IEA’s work on emerging-market smart grids makes a similar point. Newer systems do not always have to repeat the design errors of older ones.

Examples are beginning to pile up. Rwanda has provided 4G mobile phone coverage to 95% of its territory within four years and now hosts Zipline, the medical-delivery drone operator that began in Kigali in 2016 and has since deployed in Walmart’s U.S. supply chain. Kenya derives nearly half its electricity from geothermal sources in the Rift Valley and runs M-Pesa, the mobile-money platform that serves over 40 million users and is expanding regionally, a textbook case of skipping legacy banking infrastructure entirely.

Morocco’s Noor Ouarzazate complex, the world’s largest concentrated solar power plant, has set the pace for utility-scale renewables on the continent. India’s RDSS programme is a reminder that digitalisation and grid strengthening are increasingly being treated as one investment programme rather than two. UN trade agency work highlights East African dry-port and trade-facilitation initiatives in Kenya and Ethiopia as part of efforts to cut congestion and improve trade flows.

None of this means emerging markets are easier. Political risk, currency risk, procurement weakness and affordability constraints are all real. As Cecilia Mwangi, a Kenyan solar entrepreneur quoted in a Primer Africa profile, observed: “Financing is the biggest barrier. The market is there, but the funds are not.”

It does mean the retrofit burden can sometimes be lighter and the design freedom greater. That is why leapfrogging remains more than a conference cliché.

The Cost Of Delay Is Rising Faster Than The Cost Of Capital

The real danger is not that governments or investors will ignore smart infrastructure altogether. It is that they will keep underfunding it in small, politically convenient ways that gradually erode performance. A recent engineering policy review warned that without timely intervention, emergency outages, unplanned repairs and wider disruption will become more frequent across transport, water and flood-defence systems. The IEA says underinvestment already leaves electricity systems exposed to inefficiencies, losses, congestion and outages.

Deferred maintenance is no longer just a technical nuisance. It is an economic drag.

Transport and logistics offer a particularly sharp warning. The IEA notes that congestion-management costs tripled in certain advanced economies between 2019 and 2022. UN Trade and Development says waiting times at some major ports rose sharply as shipping routes were disrupted and volumes were rerouted. ACI, for its part, speaks openly about the weakened financial health of airports even as passenger demand is expected to keep climbing.

That is the underinvestment trap in a nutshell. Assets still exist, but they become more brittle, less efficient and more expensive to run.

For all the focus on capital flows, the harder constraint on smart infrastructure may turn out to be people. The IEA estimates that the global grid workforce of around 8 million will need to expand by 1.5 million by 2030 under existing policy settings, and considerably more in scenarios that meet emissions goals in full.

A joint study by Kearney and IEEE concludes the global power sector alone will need between 450,000 and 1.5 million additional engineers by 2030, with 40% of power executives already reporting difficulty hiring skilled workers. Andre Begosso, the Kearney partner who led the study, framed the stakes: “Without enough engineers, these critical projects will be delayed, compounding reliability risks and slowing the energy transition at the exact moment when momentum is needed most.”

Construction is just as exposed. The Associated Builders and Contractors put the U.S. construction labour gap at roughly 499,000 net new workers needed in 2026. The National Center for Construction Education and Research projects that approximately 41% of the current U.S. construction workforce will retire by 2031. A 2024 industry survey found nearly 90% of construction firms reported difficulty filling skilled positions.

The U.S. is forecast to face roughly 80,000 vacant electrician positions, and the HVAC sector is short 110,000 workers, a number expected to double within five years. ABC’s Anirban Basu told ENR in January 2026 that workforce shortages remain “acute enough to threaten schedules across most segments, particularly data centers, industrial megaprojects and large public works, where shortages of specialized trades — notably electricians and mechanical workers — have become binding constraints on delivery.”

The smart infrastructure layer is making the bottleneck worse, not better. Data centre commissioning, OT cybersecurity, digital twin engineering, predictive analytics and grid-edge software all draw from a small pool of specialists who are also being courted by technology, defence and clean-energy sectors.

For investors, the read-across is straightforward. Project pipelines that look bankable on paper can stall on the ground if they cannot secure electricians, commissioning engineers, controls specialists or grid planners. Schedule risk is increasingly a labour question, not just a permitting or supply-chain one.

Cybersecurity Is The New Operational Risk

Once smart infrastructure is wrapped in digital systems, a second set of risks appears: cyber resilience, data governance, interoperability and vendor dependence. The numbers here have moved from background noise to headline material.

According to Forescout’s analysis of 2024 utility data, U.S. utilities faced 1,162 cyberattacks in that year, a near 70% jump from 689 attacks in 2023. By Q3 2024, Check Point Research had recorded a 234% year-on-year increase, averaging 1,339 weekly incidents.

The case studies are no longer abstract. In October 2024, American Water, the largest regulated U.S. water utility, serving more than 14 million people across 14 states, detected a cyberattack that forced it to disconnect customer portals and pause billing. The Municipal Water Authority of Aliquippa, Pittsburgh, had to shut down operational technology after the Iran-linked group “Cyber Av3ngers” compromised one of its booster stations, defacing the human-machine interface on Israeli-manufactured Unitronics PLCs.

IBM’s 2024 Cost of a Data Breach report put the average total cost of a data breach in the industrial sector at $5.56 million, up 18% on 2023. As Mandiant’s Keith Lunden noted in the same analysis: “We expect these attacks to continue for the foreseeable future given the lack of dedicated cybersecurity personnel for many small- and mid-sized organizations operating OT.”

Physical-cyber crossover is becoming more visible too. Risk & Insurance’s late-April 2026 analysis noted that one tanker passage linked to sanctions-evading networks cut five submarine cables, leaving the Estlink 2 electricity cable between Finland and Estonia out of service for more than seven months and accumulating $70 million in repair costs.

Attacks on the U.S. telecommunications sector have increased fourfold since 2021, according to the World Economic Forum’s Global Cybersecurity Outlook 2026. Trustwave’s 2025 data recorded an 80% year-on-year surge in ransomware attacks in energy and utilities, with 84% starting via phishing.

For investors and operators, the implication is stark. A smart-infrastructure asset is only as valuable as its weakest authentication protocol. Cyber hardening, redundancy, OT segmentation and supply-chain controls are no longer optional add-ons. They are core to the asset’s operating thesis.

Smart infrastructure can raise productivity, but it also raises the penalty for poor digital governance. That makes disciplined execution every bit as important as headline spending.

The Investment Thesis Has Moved Beyond Concrete

So where does that leave the theme? It leaves it looking less like a fashionable subcategory and more like an organising principle for the next era of infrastructure finance. The winning assets are unlikely to be those that merely enjoy scarcity value or regulatory protection. They are more likely to be the ones that combine essential-service characteristics with richer operating data, higher resilience, stronger throughput, clearer upgrade pathways and credible decarbonisation logic.

McKinsey already describes infrastructure as an expanding ecosystem where digital and traditional assets are increasingly intertwined. The future built environment, on this reading, will be responsive, predictive, modernised and interdependent. Those descriptions may sound lofty, but they map directly onto investment realities already arriving in roads, ports, grids, rail and water systems.

There is one further point worth making. As Luba Nikulina, chief strategy officer of IFM Investors, told the McKinsey LA summit, infrastructure remains a “trajectory of interest” for institutional investors, with return expectations significantly elevated over the past year. But Jonathan Elkind, senior advisor at WestExec Advisors and former U.S. Department of Energy assistant secretary for international affairs, cautioned at the same event about “uncertainty around legal structures that were once thought to be beyond question,” warning that “ill-considered change can be dangerous and chilling to investment.”

That tension, between rising appetite and fragile policy frameworks, is the most important variable in the smart-infrastructure trade over the next five years.

For construction professionals, investors and policymakers, that changes the working question. The issue is no longer whether infrastructure will become smarter. It plainly will. The harder question is who captures the value created when physical assets are paired with better data, better maintenance, better software and better finance.

Countries and operators that produce credible project pipelines, open standards, sensible procurement rules and bankable risk-sharing frameworks will attract capital more easily. Those that treat digital capability as a cosmetic add-on will struggle.

Smart infrastructure investment, then, is not just another future infrastructure market story. It is becoming the practical route by which global infrastructure stays investable, operable and politically defensible in a tighter, hotter and more electrified world.