The Next Frontier of Equipment Procurement

For most of the industry’s history, acquiring a bulldozer or excavator was a reasonably contained transaction. A contractor sized up a machine against the job, negotiated a price with a dealer, arranged finance and took delivery, confident their construction equipment asset would earn its keep for a decade and hold a predictable share of its value at the end. That version of the decision has quietly been retired.

The machine still matters, but it now sits inside a far larger calculation that takes in data rights, software access, cyber exposure, charging infrastructure, emissions compliance, insurance terms, dealer service commitments and the residual risk that a diesel asset might depreciate faster than anyone expected. Purchasing has shifted from a one-off capital event into an ongoing commercial relationship, and the businesses that understand that are building very different fleets from those still buying on sticker price.

The stakes behind that shift are considerable, because equipment is typically the second-largest cost line on a construction business after labour, and the way a fleet is acquired now shapes cash flow, tender competitiveness, uptime and exposure to a moving regulatory landscape. Fleet managers are being asked to justify acquisitions not against purchase price but against total cost across a machine’s whole working life, and to defend those numbers to finance directors who have watched interest rates, insurance premiums and residual values all move at once.

For investors and lenders, the same forces are reshaping where value sits in the sector, pushing capital towards rental platforms, captive finance arms, aftermarket parts, connected-services revenue and the data that ties them together. This is no longer a story about Caterpillar versus Komatsu. It is a story about why buying heavy equipment has become one of the most complex investment decisions a contractor makes, and about the new rulebook that governs it.

Briefing

- Ownership has given way to usership, with the American Rental Association reporting that rental penetration reached a record 59.5% in 2025, a fifth consecutive annual rise as contractors preserve capital and transfer residual risk.

- Total cost of ownership, not purchase price, has become the decisive figure, and it now folds in finance, energy, software, cyber, insurance, downtime and expected resale value across a decade.

- A purchase made today locks a contractor into an emissions standard, a digital ecosystem, a software cost base, a finance structure and a resale market that will all still be running in 2035.

- Procurement has turned finance-led and data-led rather than engineering-led, with telematics, predictive maintenance and, increasingly, AI shaping which machine gets bought.

- The manufacturers themselves are becoming technology and services businesses, and capital markets increasingly value recurring software, aftermarket, finance and rental revenue over cyclical machine sales.

The fleet of 2030 starts with today’s purchase

The most important thing to understand about a purchase made now is that it is a decade-long commitment dressed as a single transaction. A machine bought this year will, in all likelihood, still be working in 2035, and everything chosen at the point of sale travels with it. The emissions standard of its engine will determine which cities and which publicly funded projects it can enter as low-emission zones tighten. The telematics and software ecosystem it ships with will dictate how it is managed, maintained and integrated with the rest of the fleet.

The finance structure will shape cash flow for years, and the brand, specification and compliance status will set the residual value a contractor eventually recovers. None of these can be meaningfully changed after delivery, which is why the buying decision now carries far more weight than the price negotiation suggests.

This lengthening of the decision horizon is what separates sophisticated buyers from the rest. A machine that looks like a bargain today can become a liability if it cannot meet a Stage V requirement in 2030, if its data is locked inside a system the fleet is moving away from, or if its diesel powertrain ages into a secondary market that has turned against it. Conversely, a slightly more expensive machine with an open data interface, a strong dealer network and a powertrain aligned with where regulation is heading can quietly outperform across its life.

The practical discipline is to buy for the fleet a contractor expects to be running at the end of the decade rather than the one they operate today, and to treat emissions trajectory, digital compatibility, financeability and resale prospects as first-order questions rather than details to settle once the model has been chosen.

From ownership to usership

The clearest change in how equipment is bought is that a growing share of it is not being bought at all. Renting, once reserved for demand peaks or specialist kit a contractor would rarely touch, has become a structural part of fleet strategy. The American Rental Association, working with S&P Global, reported that its rental penetration index rose to a record 59.5% in 2025, the fifth consecutive year of increases, and forecast continued if moderate growth into 2026.

The logic is straightforward and increasingly hard to argue against, because renting converts a capital outlay into an operating expense, preserves liquidity for labour and materials, aligns cost with project timelines and transfers residual-value risk to the rental company at a moment when the resale value of diesel machines is harder to predict. For contractors working project to project, that flexibility carries real balance-sheet value.

What has strengthened the case further is that rental fleets are now often newer, better maintained and more emissions-compliant than a contractor’s own iron. Rental houses have invested heavily in telematics, digital booking platforms and, increasingly, electric and low-emission machines, which means renting can be the fastest route to meeting a client’s sustainability requirement or a city’s emissions rule without committing capital to an asset class still finding its residual footing.

The result is a spectrum of models rather than a binary choice: outright purchase for high-utilisation core machines, rental for variable demand and specialist tasks, and a growing middle ground of rental-purchase, operating leases and fleet-management contracts. The intelligent question is no longer whether to own or rent, but which machines justify ownership on utilisation grounds and which are better accessed as a service.

Representative scenario – A European civils contractor rebalances its fleet

Consider a mid-sized European civil-engineering firm that, a decade ago, owned roughly four-fifths of its fleet outright and treated machine ownership as a mark of stability and capability. Facing tightening urban emissions rules, less predictable residual values on its ageing diesel machines and a finance director demanding sharper capital discipline, the firm moves towards a roughly even split between owned and rented equipment.

High-utilisation core machines that work across the year stay owned, while specialist and variable-demand kit shifts to rental, giving the business access to newer, emissions-compliant and electric machines without tying up capital in assets whose residuals are uncertain. The rebalancing frees working capital for labour and materials, sharpens the firm’s ability to bid for low-emission-zone projects, and moves residual risk onto rental partners. It mirrors the wider European pattern, where rental penetration has climbed year after year and tightening environmental rules have pushed the region towards asset-light models.

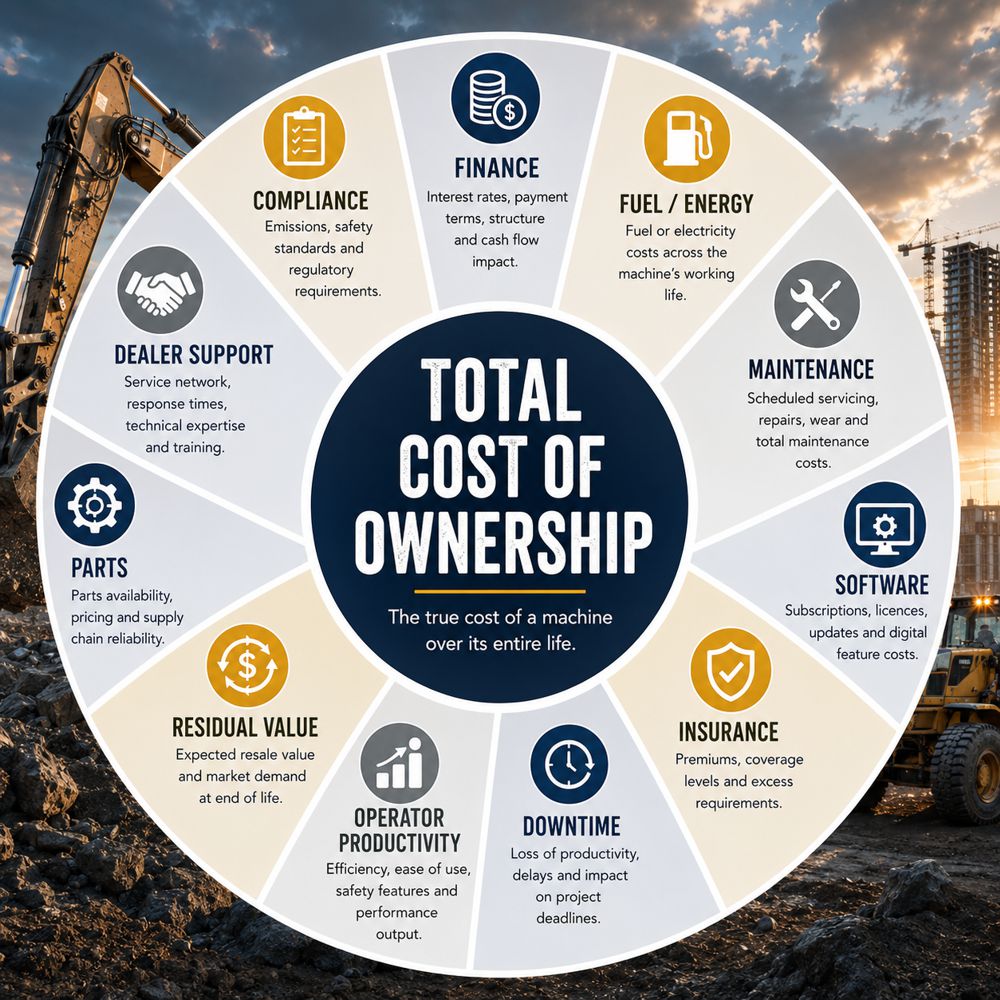

Total cost of ownership becomes the number that matters

The purchase price of a machine has always been the most visible figure and the least representative one, and it has now been firmly displaced in serious procurement by total cost of ownership. That discipline adds up acquisition, finance charges, fuel or electricity, maintenance and parts, telematics and software fees, insurance, operator productivity, downtime and eventual resale value, then divides the whole by the hours the machine is expected to work. The individual inputs have all become more volatile, which is precisely why the framework has gained authority.

Maintenance and parts costs have risen, insurance has climbed, financing is more expensive than it was before 2022, and residual values are no longer the dependable backstop they once were. A machine that looks cheap on day one can prove expensive across a five-year life, while a premium machine with lower running costs and stronger resale can quietly win.

Industry bodies have responded by making the analysis easier to run, with the European Rental Association, for instance, publishing free online calculators that model both total cost of ownership and the carbon output of construction machinery, reflecting how closely cost and emissions are now linked. Adopting this lens changes behaviour in ways that ripple through the whole acquisition. It rewards fuel and energy efficiency, favours machines with predictable service intervals and transparent parts pricing, and puts a hard number on downtime that turns dealer support and parts availability into commercial rather than operational concerns.

It also exposes the true cost of connected-machine subscriptions, insurance loadings and finance terms, which are easy to overlook at the point of sale but accumulate across a fleet and a decade. For fleet managers, mastering total cost of ownership has become the core competence; for manufacturers and dealers, being able to demonstrate a favourable lifetime cost has become a genuine competitive weapon.

Why contractors are becoming fleet data companies

One of the deeper shifts behind the new rulebook is that equipment purchasing has stopped being led by engineering and started being led by finance and data. Most machines now leave the factory able to report location, hours, fuel consumption, idle time, fault codes and productivity, and that stream of data has become central to how fleets are managed and valued.

The obstacle for years was fragmentation, because every manufacturer ran its own proprietary system and a mixed-brand fleet meant logging into a different portal for each marque. The ISO 15143-3 standard, developed from the Association of Equipment Management Professionals‘ AEMP 2.0 work and now maintained under ISO, was designed to solve exactly that by defining a common schema that lets OEM and third-party platforms exchange a consistent set of machine parameters. In practice a fleet manager can now pull location, hours, fuel use and fault data from many brands into a single dashboard rather than stitching together fragmented exports.

That capability is turning contractors into something closer to data companies that happen to move earth. Predictive maintenance, in particular, has moved from concept to competitive necessity, with machine-learning models trained on fleet-wide failure patterns monitoring live telematics and flagging component degradation before it becomes a breakdown, allowing repairs to be scheduled into planned downtime rather than emergency windows.

The predictive-maintenance market is projected by several analysts to grow from around 10.9 billion US dollars in 2024 to more than 70 billion by 2032, a pace that reflects how quickly the approach is being adopted, and reported downtime reductions in early construction deployments are substantial. Alongside it, utilisation analysis identifies which machines are earning and which are idle, benchmarking compares performance across a fleet and against peers, and digital twins, continuously updated virtual replicas that combine sensor data with simulation, are beginning to model how assets behave over their lives.

The commercial implication for buyers is that data interoperability now belongs on the purchase specification beside horsepower and bucket capacity, because a machine that reports cleanly through an open standard is easier to maintain, easier to benchmark and easier to sell with a documented history, while one locked into a closed system carries a hidden cost that compounds.

Representative scenario – A North American contractor designs out downtime

Picture a North American earthmoving contractor running a mixed fleet of connected excavators and haulers. Historically it serviced machines on a calendar schedule and absorbed the occasional catastrophic failure mid-project, each one idling crews and threatening milestones. By feeding live telematics, engine temperatures, hydraulic pressures, fuel anomalies and fault codes, into machine-learning models trained on fleet-wide failure patterns, the contractor begins catching component degradation hundreds of operating hours before it becomes a breakdown, scheduling repairs into planned windows rather than emergencies.

The shift turns maintenance from a reactive gamble into a managed cost and protects the uptime on which project margins depend. The direction is industry-wide and no longer speculative: Caterpillar alone reports a fleet of more than 1.6 million connected, reporting assets underpinning predictive maintenance and AI-assisted fleet tools, and the global predictive-maintenance market is projected to grow from around 10.9 billion US dollars in 2024 to over 70 billion by 2032.

When an algorithm shortlists the machine

The next stage of this shift is already visible, as artificial intelligence begins to move into the purchasing decision itself. The logic of total cost of ownership is fundamentally a data problem, and data problems are precisely what modern AI systems are built to solve. It is not difficult to imagine a fleet manager posing a query in plain language, the lowest total-cost-of-ownership 35-tonne excavator for six thousand annual hours in southern Spain, say, and receiving a ranked recommendation assembled from dealer pricing, fuel and energy costs, maintenance histories, resale curves, finance rates and utilisation patterns.

Elements of this already exist in fleet-analytics platforms, and the trajectory is towards systems that generate purchasing shortlists automatically rather than requiring a human to build the model by hand. Autonomous workflows that detect a fault, order the part and schedule the technician without human intervention are moving from pilot into production, and the same underlying capability points naturally towards automated acquisition analysis.

The effect on the profession will be significant without being straightforwardly threatening. As AI takes over the calculation, the fleet manager’s role shifts from calculator to decision validator, the person who interrogates the model’s assumptions, weighs the factors an algorithm cannot see and owns the judgement that follows. Local knowledge, dealer relationships, operator preferences, project-specific constraints and an understanding of where regulation is heading remain human contributions that a recommendation engine cannot fully capture.

For manufacturers and dealers, this raises the stakes on data transparency, because a machine whose true lifetime cost is visible and favourable will surface in automated shortlists, while one whose economics are opaque risks being filtered out before a human ever considers it. The businesses that prepare now by structuring their maintenance and cost data are, in effect, building the raw material on which the next generation of procurement decisions will run.

Software subscriptions and the connected machine

As machines have become more connected, manufacturers have moved parts of the value proposition into software, and buyers are learning to read the subscription line as carefully as the specification sheet. Grade control, machine guidance, fleet-management portals, advanced telematics tiers and remote diagnostics are increasingly delivered as recurring services rather than one-time features baked into the purchase.

For manufacturers and dealers this is a deliberate and defensible strategy, since connected-services and aftermarket revenue is steadier and higher-margin than machine sales, and it funds the continued development of the very software that makes modern equipment productive. For the wider sector it signals a shift in where value accrues, which is one reason investors increasingly prize recurring digital and aftermarket income streams within equipment businesses.

For contractors, the arrival of subscriptions demands a sharper eye at the point of purchase and across the ownership period. A machine bought outright may still depend on active subscriptions to unlock features that were central to the buying decision, and those fees, multiplied across a fleet and compounded over years, feed straight into total cost of ownership.

The practical response is to treat software terms as part of the negotiation by establishing which capabilities are permanent and which are rented, how pricing may change over the machine’s life, whether data and functionality remain accessible if a subscription lapses, and how the arrangement transfers to a second owner. Handled well, connected services genuinely lift productivity and uptime and can more than pay for themselves. Handled without scrutiny, they become a quiet, recurring cost that erodes the economics the buyer thought they had secured, and they raise a question the industry is only beginning to confront directly: what exactly does a contractor own when much of a machine’s capability lives in software controlled by someone else.

Cybersecurity and who really controls the machine

A connected machine is a computer that happens to dig, and like every computer it represents an attack surface. This is one of the least discussed dimensions of modern equipment buying and one of the fastest rising. As excavators, loaders and haulers acquire cellular connectivity, cloud back-ends, over-the-air software updates and remote-diagnostic access, they inherit the vulnerabilities that come with all of those things.

The parallel with the automotive sector is instructive, where researchers documented several hundred publicly reported cybersecurity incidents across the connected-vehicle ecosystem in 2025, with the majority conducted remotely and a large share touching telematics or cloud infrastructure rather than requiring physical access. The off-highway world has not yet seen incidents on that scale reported publicly, but it runs on the same architecture, and the frameworks emerging in automotive, including the UN’s cybersecurity and software-update regulations and the ISO/SAE 21434 engineering standard, indicate the direction of travel for connected machinery more broadly.

For buyers, this turns a set of previously invisible questions into legitimate points of due diligence. Who owns the data a machine generates, and where is it stored. Can a machine be remotely disabled, and if so, by whom and under what circumstances. What happens to functionality and data if a subscription lapses or a manufacturer changes its terms. How are over-the-air updates secured against tampering, and what is the manufacturer’s track record on disclosing and patching vulnerabilities.

These are not fringe concerns, because a compromised fleet-management system or a spoofed software update could halt a site as effectively as a mechanical failure, and the concentration of data and control in manufacturer back-ends means the risk is systemic rather than machine-by-machine. The mature response is not to retreat from connectivity, which delivers real value, but to make security posture and data governance part of the buying conversation, asking manufacturers to be explicit about ownership, access, resilience and control before the contract is signed.

Uptime economics: dealers, parts and the right to repair

Once total cost of ownership puts a price on downtime, dealer support and parts availability stop being back-office considerations and become central to the buying decision. A machine is only as good as the network that keeps it running, and contractors are increasingly weighing service response times, technician coverage, parts stocking and warranty terms as heavily as the specification itself.

This has sharpened attention on a debate that has migrated from agriculture into construction: the right to repair. Modern machines rely on embedded software and dealer-controlled diagnostic tools, and some repairs require a manufacturer-authorised digital handshake before a machine will return to service. When that access is restricted, owners can face longer waits and higher bills, which is precisely the cost that uptime-focused buyers are trying to design out.

The issue has moved decisively over the past eighteen months, and the direction of travel favours the buyer. In January 2025 the United States Federal Trade Commission, joined by state attorneys general, filed suit against John Deere over restricted access to repair software, and Deere separately settled a class action, agreeing to pay farmers around 99 million US dollars and to make diagnostic and repair tools available to owners and independent shops for roughly a decade.

Deere and other manufacturers have expanded self-service diagnostic access, in some cases through subscription platforms, and comprehensive right-to-repair laws have passed in several US states including Colorado and Minnesota, with a federal proposal introduced in late 2025. Manufacturer bodies such as the Association of Equipment Manufacturers and dealer associations continue to caution that unrestricted access to embedded code could compromise safety and emissions compliance, and that legitimate concern is shaping how access is delivered rather than whether it expands. For buyers, the takeaway is constructive, because repair-tool access, parts commitments and service coverage are now fair game in negotiations, and the market is trending towards greater transparency on all three.

The rise of fleet standardisation

A quieter but consequential change in how large contractors buy is that many are deliberately narrowing the number of manufacturers they deal with. The instinct to chase the best individual machine for each task is giving way to a recognition that a standardised fleet is often cheaper and easier to run across its whole life. Buying from fewer OEMs simplifies technician training, because mechanics become genuinely expert on a smaller range of systems rather than passably familiar with many. It shrinks the parts inventory a business must hold and the number of supplier relationships it must maintain. It makes telematics and software integration far less painful, since data flows more cleanly when machines share a platform, and it eases a real operational headache, because cross-trained technicians able to service many brands are scarce, particularly in Europe where rental and contractor fleets draw from many OEMs, each with its own proprietary diagnostics. And it builds operator familiarity, so crews move between machines without relearning controls, which lifts productivity and reduces the risk of error.

The trade-off is real, and it is a trade the market is increasingly willing to make. Standardising on fewer brands may mean occasionally accepting a machine that is not the outright best in class for a particular job, in exchange for lower training costs, simpler maintenance, cleaner data integration and stronger purchasing leverage with a smaller group of suppliers. In quarrying and other high-utilisation, maintenance-intensive operations, where uptime is everything and technicians service the same machines day after day, the standardisation logic is especially strong, and consolidating on a single OEM’s earthmoving line can measurably reduce maintenance complexity and cost.

For manufacturers, this raises the value of breadth and of a compelling digital ecosystem, because winning a place on a contractor’s shortlist increasingly means winning the whole fleet relationship rather than a single sale, and losing it means being designed out across the board. The dynamic rewards OEMs that can offer a coherent range, consistent data standards and dependable support, and it pressures those whose strength lies in one or two standout products but who cannot support a contractor across the full spread of a modern fleet.

Insurance, theft and the new arithmetic of risk

Insurance has become an active input into the buying decision rather than a cost to be settled afterwards, and telematics is the reason. Insurers increasingly price construction equipment on the basis of how well it is monitored and protected, taking into account GPS tracking, geofencing, immobilisers, operator-behaviour data and site security when calculating premiums. A machine specified with robust connected security can attract better terms than one without, which means the choices made at purchase feed directly into the cost of insuring the asset across its life.

This is a meaningful shift, because it rewards buyers who treat security and connectivity as core specification rather than optional extras, and it further blurs the line between a machine’s physical attributes and its digital ones.

The backdrop is a theft problem that carries real cost. Industry estimates put the annual cost of construction and plant theft in the United Kingdom at more than a billion pounds, with figures widely cited of over eleven thousand reported thefts a year, the overwhelming majority of firms affected at some point, and a recovery rate below a quarter, dramatically lower than the recovery rate for stolen cars.

The European Rental Association has estimated that tens of thousands of heavy machines and hundreds of thousands of smaller tools are stolen across Europe each year. The most effective single measure for recovery is telematics, since GPS-tracked machines with geofencing and motion alerts are recovered at far higher rates and often within hours, while the true cost of a theft extends well beyond the asset to idle labour, hired replacements at premium rates, schedule penalties and the multi-year premium increases that follow a claim.

For buyers, the arithmetic is clear enough to shape specification, because connected security lowers both the likelihood of loss and the cost of cover, and it does so while delivering the utilisation and maintenance benefits that justified telematics in the first place.

Residual values, the used market and the auction houses

Resale value has always been the quiet determinant of ownership economics, and it demands more attention than usual because the numbers are moving. After the extraordinary run-up that followed the pandemic, used prices have been normalising, and data from Ritchie Bros. and Rouse showed used resale and auction values softening through 2025 before a more mixed picture emerged in early 2026, with earthmoving categories holding their pricing better than aerial equipment and telehandlers.

This is a market finding a healthier level after an unusual period rather than a market in distress, and it cuts in different directions depending on which side of the transaction a business sits. For buyers, softer used prices open a genuine window of better value and stronger negotiating leverage, particularly as OEM certified-used programmes and digital inspection bring documentation and confidence to what was once an opaque corner of the market. For sellers, timing and the factors that preserve value, brand strength, verified low hours, complete telematics-backed service records and emissions compliance, matter more than ever, because an ageing diesel machine facing tightening city rules can depreciate faster than its hour-meter alone suggests.

Underpinning this whole market is an infrastructure of auction houses and marketplaces that has become central to how equipment is valued, bought and sold, and it is worth understanding as part of the procurement picture. RB Global, the parent of Ritchie Bros. and formerly known by that name since its founding in 1958, reported total revenue of around 4.28 billion US dollars and gross transaction value of roughly 15.9 billion in 2024, operating an omnichannel network that spans live auctions, the IronPlanet online marketplace with its condition-certification service, the Marketplace-E controlled marketplace, the Mascus listing platform and the Rouse valuation and data business.

That reach means the sector now has genuine price transparency, with free access to more than a million past auction results allowing any buyer or seller to benchmark a machine’s likely value before committing. Euro Auctions and other specialists add further liquidity, and the combined effect is a used market that is faster, more data-rich and more international than it was a decade ago. For buyers, this changes the residual calculation from guesswork into something closer to a modelled input, and it makes the exit strategy for a machine part of the decision to acquire it in the first place.

Can Chinese manufacturers change the buying equation?

No account of how equipment buying has changed would be complete without the rise of the Chinese manufacturers, whose growing international presence is reshaping competition at the point of sale. SANY, XCMG, LiuGong and Zoomlion have moved from serving their vast domestic market to exporting at scale, and the numbers behind that expansion are striking. XCMG has been ranked among the top handful of global manufacturers, with reported 2024 revenue in excess of 13 billion US dollars and a presence across more than 180 countries, while SANY sits among the largest producers worldwide and is a global leader in concrete pumps, operating in more than 150 countries.

Chinese construction-machinery exports to Africa reportedly grew by over half in 2025, and the leading firms have built research centres, assembly plants and parts-and-service networks abroad rather than simply shipping machines. In several segments, most notably cranes and concrete pumping, Chinese manufacturers are now acknowledged among the world’s leaders.

The more important point for buyers is how this competition is being fought, because it is forcing the established OEMs to compete on terms beyond reputation. Where Western manufacturers have long relied on brand strength and proven resale value, the Chinese challengers are competing hard on price, warranty, financing, dealer support and, increasingly, technology, particularly in electrification where China’s domestic market is far ahead and electric loaders and mixer trucks have already passed half of new sales in some categories.

This pressures incumbents to sharpen their own offers on all of those fronts, which benefits every buyer whether or not they ever purchase a Chinese machine. The remaining hurdle for the challengers is perception and residual value, since resale markets still tend to reward the established brands, and a machine’s second-hand value is part of its total cost of ownership. That gap is narrowing as build quality and support networks mature, and the trajectory suggests that buyers a few years from now will weigh a genuinely global field of manufacturers, judged on lifetime cost and support rather than reputation alone.

Buying electric equipment: compliance, cost and the questions that remain

Electric equipment has become a serious procurement question rather than an environmental gesture, driven in large part by rules that increasingly decide which projects a machine can enter. London’s Non-Road Mobile Machinery Low Emission Zone, administered by the Greater London Authority, requires engines rated between 37 and 560 kilowatts on construction sites to meet minimum emissions stages, with the standard set to tighten to Stage V in 2030 and to zero-emission machinery by 2040.

Oslo has gone further, mandating zero-emission machinery on municipal construction from the start of 2025, having already reached around 85% zero-emission activity on its municipal sites by 2024, with Copenhagen, Helsinki and others following. A machine that cannot meet the rule for a given site simply cannot work there, which turns compliance into a hard commercial gate and pushes contractors bidding for urban and publicly funded work to weigh emissions capability at every acquisition.

Buying electric, though, is about far more than ticking an environmental box, and the practical considerations are where the real decision lies. Charging infrastructure is the first, because an electric fleet needs power on site, and grid constraints frequently mean temporary connections are insufficient, requiring battery energy-storage systems or on-site generation to cover demand.

Utilisation models change, since early Nordic projects found that electric fleets can require modestly more units to cover charging downtime, and cold weather affects performance. Battery degradation over time and the resulting uncertainty in the secondary market are genuine unknowns, because the industry does not yet have decades of resale data on electric machines, which complicates the residual side of any total-cost calculation. Government incentives are helping to bridge the upfront cost, including national schemes such as the Netherlands’ clean-machinery subsidy programme, and the operating economics are increasingly favourable, with lower energy and maintenance costs and the ability to work extended or indoor hours thanks to reduced noise and zero local emissions.

Research such as Volvo and Skanska’s electric-quarry trials at Vikan Kross in Sweden has pointed to the potential for materially lower total operating costs and a near-total cut in site carbon emissions once electrification is designed into a whole site, which is the strongest signal yet that compliance and cost efficiency are beginning to converge. For buyers, the sensible path is often to use rental to gain electric experience and meet immediate requirements while residual values mature, and to reserve outright purchase for applications where the utilisation and charging picture is well understood.

Case study – Oslo, Norway: an all-electric heritage renovation

Oslo’s Sophies Minde project, documented by the International Council on Clean Transportation, shows what buying electric looks like in practice. Realising the city’s 2025 mandate for zero-emission municipal construction, the project ran an all-electric fleet of excavators, wheel loaders, cranes, drills and pavers to convert a former hospital into a community centre, and by mid-2024 had cut emissions by more than 200 tonnes of CO2 equivalent by replacing diesel machines. The operational learnings are as valuable as the headline figure.

The project manager estimated that electric machines required roughly 10 to 15% more units on site to match diesel capacity because of charging downtime, a gap expected to narrow as battery technology improves, and during one exceptionally cold spell, with temperatures near minus 25 degrees Celsius, battery capacity fell by around 40%. The machines nonetheless met demanding performance requirements across most conditions, demonstrating that electric equipment is viable today while reshaping how a fleet must be sized and scheduled.

Case study – The Gulf: electric pilots and milestone rentals on the giga-projects

The Gulf’s giga-projects are reshaping procurement in two directions at once. On sustainability, Volvo Construction Equipment put its first zero-emission machines to work in the United Arab Emirates during the country’s 2023 Year of Sustainability, deploying a compact ECR25 Electric excavator, a 23-tonne EC230 Electric excavator and an L120 Electric wheel loader on a customer site, a signal that electric power is arriving even in a market defined by scale and heat.

On the commercial side, contractors on Saudi Arabia’s giga-projects, part of a Vision 2030 pipeline running well into the trillions of dollars, are increasingly favouring variable-rate rentals tied to project milestones rather than outright purchase, preserving flexibility across multi-year programmes. The nuance is instructive, because on remote sites without grid access, advanced diesel machines still often win on practicality, underlining that the modern buying decision turns on fit, support and total cost rather than technology for its own sake.

The investor’s lens: manufacturers become technology businesses

The way capital markets assess this industry has shifted in step with the way contractors buy, and the clearest sign of it is visible in how the market now values the manufacturers themselves. Investors increasingly reward recurring, higher-margin income from services, aftermarket parts, software, finance and rental over the cyclical, lumpy revenue of machine sales, and the major OEMs have restructured around that reality. Caterpillar, which reported sales and revenues of 67.6 billion US dollars in 2025, has made growing its services business an explicit multi-year priority, lifting services revenue to around 24 billion and targeting roughly 28 billion, on the logic that aftermarket parts, repairs, equipment management and performance contracts carry higher margins and prove far less volatile than new-equipment orders through the cycle.

That business rests on a fleet of more than 1.6 million connected, reporting assets that feed predictive maintenance, fleet management and AI tools, and on a financial-products arm offering financing, leasing and insurance. The same logic runs through the sector: Deere has built recurring revenue around precision technology and its digital operations platform, Komatsu around its Smart Construction and electric offerings, and Volvo CE around electric-equipment leadership and financial services. These businesses are, increasingly, technology and services companies that happen to manufacture machines, and analysts now track the services share of revenue as closely as unit sales.

That reframing flows straight back to the contractor, because fleet quality has quietly become a financial metric. Investors and financiers increasingly reward companies that run younger fleets, since a younger fleet implies lower maintenance risk, better emissions compliance and stronger residual backing, and they value predictable total cost of ownership, higher utilisation and sophisticated digital fleet management because those characteristics translate into steadier cash flow and lower operational risk. They also weigh emissions profile, both because it determines access to a widening pool of regulated work and because it signals exposure to stranded-asset risk as rules tighten.

A contractor whose fleet is old, poorly monitored and heavily diesel is not merely operationally weaker; it is, to a lender or investor, a riskier proposition. The Equipment Leasing and Finance Foundation projected real equipment and software investment to grow by around 6% in 2026, with fleet replacement and modernisation rather than expansion as the primary drivers and industry confidence holding above its long-run average, a backdrop that rewards disciplined, data-led acquisition. Captive finance arms of the major manufacturers remain central to how machines are funded, competing with banks and newer fintech lenders, and the structure of that finance increasingly reflects the quality of the asset and the sophistication of the buyer. The message for contractors is that buying well is no longer only about running an efficient site; it is about being the kind of business that capital wants to back.

How Equipment Procurement Could Look by 2035

One of the clearest developments is the gradual shift towards Equipment-as-a-Service rather than outright ownership. Manufacturers are already expanding subscription-based software, connected fleet management, predictive maintenance and financial services alongside traditional equipment sales. It is a relatively small step from selling a machine to selling guaranteed availability, productivity or operating hours. Contractors may increasingly pay for performance rather than ownership, with finance, servicing, software updates, telematics and maintenance bundled into long-term agreements that provide predictable monthly costs instead of large capital purchases. Several manufacturers are already experimenting with uptime guarantees, performance contracts and subscription-based digital services, suggesting that the transition has already begun rather than remaining a theoretical possibility.

The industry is only beginning to understand how profoundly equipment procurement is changing. Many of the commercial models emerging today are likely to become standard practice over the next decade, reshaping not only how contractors acquire machinery but how manufacturers design, finance and support it throughout its working life. While diesel-powered excavators and wheel loaders will remain familiar sights on construction sites, the commercial model surrounding them may look very different.

Artificial intelligence is also likely to become an increasingly influential participant in procurement decisions. Today’s fleet-management platforms already analyse utilisation, maintenance schedules and fuel consumption, but future systems are expected to combine live operating data with dealer inventories, finance rates, residual-value forecasts and project requirements to recommend the most economical acquisition strategy automatically.

Rather than asking which excavator to buy, fleet managers may ask an AI platform to identify the most cost-effective solution for a specific project, with recommendations balancing ownership, rental and leasing options simultaneously. Procurement professionals will remain central to the process, but their role will increasingly focus on validating strategic decisions rather than manually comparing technical specifications.

Electrification will reinforce this evolution. As battery technology improves, charging infrastructure expands and zero-emission regulations become more widespread, equipment purchases will increasingly be assessed alongside energy management. Battery leasing, charging-as-a-service and integrated site-energy contracts may become as commonplace as finance agreements are today. At the same time, digital twins, autonomous fleet optimisation and predictive maintenance will continue reducing downtime while extending equipment life, creating additional value long after the initial purchase.

For manufacturers, this represents a profound change in business strategy. Success will depend less on selling the greatest number of machines and more on building long-term customer relationships through software platforms, finance, aftermarket services and data-driven productivity solutions. For contractors, the implication is equally significant. Buying equipment will become less about selecting a single machine and more about choosing the ecosystem, technology partner and commercial model that will support their business throughout the asset’s entire working life.

Ten Questions Every Contractor Should Ask Before Signing

Before committing hundreds of thousands, or even millions, to new equipment, procurement teams should be able to answer a series of straightforward but increasingly important questions. They extend well beyond horsepower, lifting capacity or purchase price, and together determine whether a machine becomes a profitable long-term asset or an expensive liability.

- Does this machine genuinely justify ownership, or would rental provide a better financial return?

- What is the realistic total cost of ownership over its expected working life?

- Will it integrate seamlessly with our existing telematics, software and fleet-management platforms?

- Which features depend on ongoing software subscriptions, and what will those subscriptions cost over the next decade?

- How strong is the dealer’s service network, and what response times and parts availability can be guaranteed?

- Will tightening emissions regulations restrict where this machine can work or reduce its future resale value?

- Who owns the operational data generated by the machine, and how secure and portable is that information?

- Does the proposed finance package match expected utilisation, cash flow and replacement strategy?

- What happens once the warranty expires, and how easily can the machine be maintained or repaired?

- Will this machine still be commercially competitive, compliant and profitable in 2035?

Businesses that can answer these questions with confidence are far more likely to make purchasing decisions that continue delivering value long after the initial transaction has been forgotten.

The New Procurement Checklist

The cumulative effect of all these changes is that the equipment buying process has been fundamentally rewritten. A decade ago, procurement was largely an engineering decision centred on selecting the best machine for the job. Today it has become a strategic business decision that combines finance, technology, regulation, cybersecurity, sustainability, data management and long-term asset planning.

The most successful contractors are no longer simply comparing excavators, loaders or dozers. They are comparing business models. They evaluate ownership against rental, lifetime operating costs against headline purchase prices, software ecosystems alongside hydraulic performance, dealer capability alongside machine specification, and future regulatory compliance alongside today’s project requirements. The purchase order has become only the beginning of a commercial relationship that may last for ten years or more.

Buying heavy equipment has therefore become one of the most complex investment decisions a construction business makes. Yet that complexity should not be viewed as a burden. It is an opportunity for better-informed organisations to gain a lasting competitive advantage. Contractors who master the new rules of procurement will build fleets that are more productive, more resilient, more sustainable and ultimately more profitable. In an industry where margins are often measured in percentages rather than tens of percentages, making smarter purchasing decisions has become every bit as important as operating the machines themselves.

The Decade Ahead

For all the change described here, it is worth holding on to a grounding truth. The excavator itself has not changed as dramatically as the business case behind it, and the fundamentals of the work remain reassuringly physical. In the coming decade, contractors will still move earth with steel and hydraulics, still rely on skilled operators and dependable dealers, and still take pride in machines that perform in the heat, the cold and the dust. What has changed is everything that surrounds the machine, and that is where the profitability of the next decade will be decided.

The decisions that determine whether a fleet makes money will increasingly be made through software, data, finance and regulation rather than through horsepower and bucket capacity alone. The companies that recognise this shift earliest will not simply own better machines. They will own more productive businesses, better positioned to win the work, secure the finance and adapt to whatever the decade brings. In an industry that has always prized substance over noise, that is the quiet revolution worth paying attention to, and the new rules of procurement are how it is already unfolding.

Key Industry Questions

- Is it better to rent or buy heavy equipment now? There is no single answer, and the strongest fleets deliberately run both. The practical test is utilisation: machines that work consistently across the year usually justify ownership, while equipment tied to variable demand, specialist tasks or short-duration projects often costs less as a rental. Renting preserves capital, converts a fixed outlay into an operating expense aligned with project timelines, and shifts residual-value risk to the rental company at a time when diesel resale values are less predictable. It also offers fast access to newer, emissions-compliant and electric machines without tying up cash or committing to an asset class whose residuals are still maturing. Ownership still wins on high-hour core assets where long-term control and cost-per-hour favour holding the iron. The decision should follow the numbers, not tradition.

- What is total cost of ownership and why has it replaced purchase price? Total cost of ownership adds every expense a machine incurs across its working life, including acquisition, finance charges, fuel or electricity, maintenance and parts, telematics and software fees, insurance, downtime and expected resale value, then measures the result against the hours worked. It has displaced purchase price because that headline figure captures only the opening moment of a relationship that runs for years, and the other inputs have become more volatile as maintenance, insurance and finance costs have risen and residual values have grown less certain. A machine that looks cheap can prove expensive once running costs, downtime and weak residuals are counted, while a premium unit with lower operating costs and stronger resale can be the better buy. Running this analysis on every significant acquisition is now the core discipline of professional fleet management.

- How is data changing the way contractors buy equipment? Purchasing has become finance-led and data-led rather than engineering-led. Machines generate continuous telematics data, and the ISO 15143-3 standard lets contractors pull consistent information across mixed-brand fleets into a single interface. That data feeds predictive maintenance, where machine-learning models flag component failures before they cause downtime, alongside utilisation analysis, benchmarking and emerging digital-twin modelling. A machine that reports cleanly through an open standard is easier to maintain, benchmark and resell with a documented history, so data interoperability now belongs on the purchase specification. Increasingly, AI is moving into the decision itself, capable of assembling total-cost-of-ownership recommendations from dealer prices, fuel, maintenance, resale and finance data, which shifts the fleet manager’s role from calculator to decision validator who interrogates the model and owns the judgement.

- What cybersecurity questions should equipment buyers ask? A connected machine is a computer with an engine, and it carries the vulnerabilities of any networked device, including cloud back-ends, over-the-air updates and remote access. The automotive sector has already seen hundreds of connected-vehicle incidents reported in a single year, most conducted remotely, and construction equipment runs on similar architecture. Buyers should ask who owns the data a machine generates and where it is stored, whether the machine can be remotely disabled and by whom, what happens to functionality and data if a subscription lapses, and how over-the-air updates are secured against tampering. These are questions of business continuity, because a compromised fleet system could halt a site as effectively as a mechanical failure. The mature response is to make security posture and data governance part of the buying conversation rather than an afterthought.

- How does the right to repair affect construction equipment ownership? Modern machines depend on embedded software and dealer-controlled diagnostic tools, and some repairs require an authorised digital process before a machine returns to service, which can lengthen downtime and raise costs. The debate has moved quickly: in early 2025 the US Federal Trade Commission and state attorneys general sued John Deere over restricted repair-software access, Deere settled a related class action agreeing to make diagnostic tools available to owners and independent shops, and several US states including Colorado and Minnesota have passed right-to-repair laws. Manufacturer and dealer bodies caution that unrestricted access to embedded code could affect safety and emissions compliance, which is shaping how access is delivered rather than halting its expansion. For buyers, repair-tool access, parts availability and service commitments are now legitimate points of negotiation, and transparency on all three is improving.

- Why are large contractors standardising on fewer manufacturers? Standardisation lowers whole-life cost in ways that a best-machine-for-every-task approach cannot. Buying from fewer OEMs simplifies technician training, shrinks the parts inventory a business must hold, eases telematics and software integration, and builds operator familiarity that lifts productivity and reduces error. The trade-off is occasionally accepting a machine that is not the outright best in its class, in exchange for cheaper maintenance, cleaner data integration and stronger purchasing leverage with a smaller group of suppliers. The logic is strongest in high-utilisation, maintenance-intensive operations such as quarrying. For manufacturers, this raises the stakes considerably, because winning a place on a contractor’s shortlist increasingly means winning the whole fleet relationship rather than a single sale, which rewards OEMs that offer a coherent range, consistent data standards and dependable support.

- How should buyers approach electric equipment beyond emissions compliance? Emissions rules increasingly gate which projects a machine can enter, but buying electric is a practical decision that extends well past compliance. Charging infrastructure is the first consideration, because an electric fleet needs adequate site power, and grid constraints often require battery storage or on-site generation. Utilisation models shift, since charging downtime can mean needing modestly more units, and cold weather reduces battery performance. Battery degradation and secondary-market uncertainty complicate residual planning, because the industry lacks decades of resale data on electric machines. Against that, energy and maintenance costs are lower, machines can work extended and indoor hours, and incentives such as national subsidy schemes offset upfront cost. Many buyers use rental to gain electric experience and meet immediate requirements while residuals mature, reserving purchase for applications where the charging and utilisation picture is well understood.

- Can Chinese manufacturers really compete on more than price? Increasingly, yes, and that is reshaping the whole buying equation. SANY, XCMG, LiuGong and Zoomlion have expanded from their domestic market to more than 150 to 180 countries each, built overseas plants and service networks, and established genuine leadership in segments such as cranes and concrete pumping. They compete hard on warranty, finance, dealer support and technology, particularly electrification, which pressures established OEMs to improve their own offers and benefits every buyer. The remaining hurdle is perception and residual value, since resale markets still tend to reward established brands and second-hand value is part of total cost of ownership. That gap is narrowing as build quality and support mature, and buyers a few years from now are likely to weigh a genuinely global field of manufacturers on lifetime cost and support rather than reputation alone.

- How does equipment finance affect buying decisions in the current market? Financing is more expensive than it was before 2022, but conditions have stabilised enough to support planned acquisition and leasing. The Equipment Leasing and Finance Foundation projected real equipment and software investment to grow by around 6% in 2026, with fleet replacement and modernisation, rather than expansion, as the primary drivers and industry confidence holding above its long-run average. Captive finance arms of the major manufacturers remain central to how machines are funded, competing with banks and newer fintech lenders. The cost of capital now swings total cost of ownership meaningfully, which makes finance structure part of the acquisition strategy rather than an afterthought. Aligning loan or lease terms with a machine’s expected working life and residual profile is increasingly where disciplined buyers protect their margins.

- Are equipment manufacturers becoming technology companies? In effect, yes, and it is changing what a purchase relationship means. The major OEMs have restructured around recurring, higher-margin revenue from services, aftermarket parts, software and finance, which carry steadier margins than cyclical machine sales. Caterpillar, with 2025 sales and revenues of 67.6 billion US dollars, has grown services revenue to around 24 billion and targets roughly 28 billion, underpinned by a fleet of more than 1.6 million connected assets and its own finance arm. Deere, Komatsu and Volvo CE are pursuing similar strategies around precision technology, connected-construction platforms, electrification and financial services. For buyers, this means a machine increasingly comes bundled with an ongoing digital and service relationship, so the manufacturer’s software roadmap, data terms and support model matter as much as the iron, and choosing a machine is partly choosing an ecosystem to live inside for a decade.

Strategic Takeaways

- A purchase made today locks a contractor into an emissions standard, a digital ecosystem, a software cost base and a resale market for the next decade, so buyers should specify for the fleet they expect to run in 2035 rather than the one they operate today.

- Total cost of ownership has become the language of serious procurement, and the businesses that master it – and the manufacturers that can demonstrate a favourable lifetime cost – hold a decisive advantage as automated, AI-led purchasing tools mature.

- The equipment manufacturers are becoming technology and services businesses, with recurring software, aftermarket, finance and rental revenue increasingly valued above cyclical machine sales, which reshapes both how machines are sold and what buyers are committing to.

- New considerations that barely existed a decade ago – cybersecurity, insurer telematics requirements, fleet standardisation and Chinese OEM competition – now shape the buying decision, and treating connected security and data governance as core specification lowers cost and risk simultaneously.

- Fleet quality has become a financial metric, with younger, well-monitored, lower-emission fleets rewarded by lenders and investors, so buying well is no longer only an operational discipline but a determinant of the terms on which capital is available.