Freight Becomes The Real Price Of Bitumen

When a chokepoint at the mouth of the Gulf seizes up, most people picture petrol pumps and jittery stock tickers. Road builders feel it somewhere less obvious, in the price of the black, sticky binder that holds their highways together. Petroleum bitumen, filed under customs code HS 271320, is barely a sliver of the oil barrel, yet it rides the same heated ships, buys the same war-risk cover and waits in the same canal queues as everything else that floats out of a refinery. So when the Strait of Hormuz tightened in early 2026, the cost of resurfacing a road in Mombasa or Mumbai began creeping upward within weeks, long before it ever showed up in a customs spreadsheet.

That’s the uncomfortable lesson buried in a fresh reading of 2024 trade data and the shocks that have rattled the market since. Bitumen isn’t traded like crude. It’s a regional, logistics-bound supply chain, and unusually exposed to freight, because the stuff has to be kept hot, shipped in specialised vessels or packed into drums and bags, and matched to road-building demand that doesn’t pause for a shipping crisis. For the engineers, financiers and ministries who treat it as a routine line item, the past two years have been a blunt reminder that bitumen behaves far more like a strategic material than a commodity afterthought.

For countries investing billions into roads, airports and logistics corridors, freight volatility increasingly dictates delivered infrastructure cost more than refinery output itself.

Briefing

- Bitumen freight now moves faster than most road budgets, so a maritime shock can reprice delivered tonnes within weeks rather than quarters.

- Four corridors dominate the trade: Canada into the United States, the Gulf into India and East Africa, Singapore into South-East Asia and Australia, and the Mediterranean into North and West Africa.

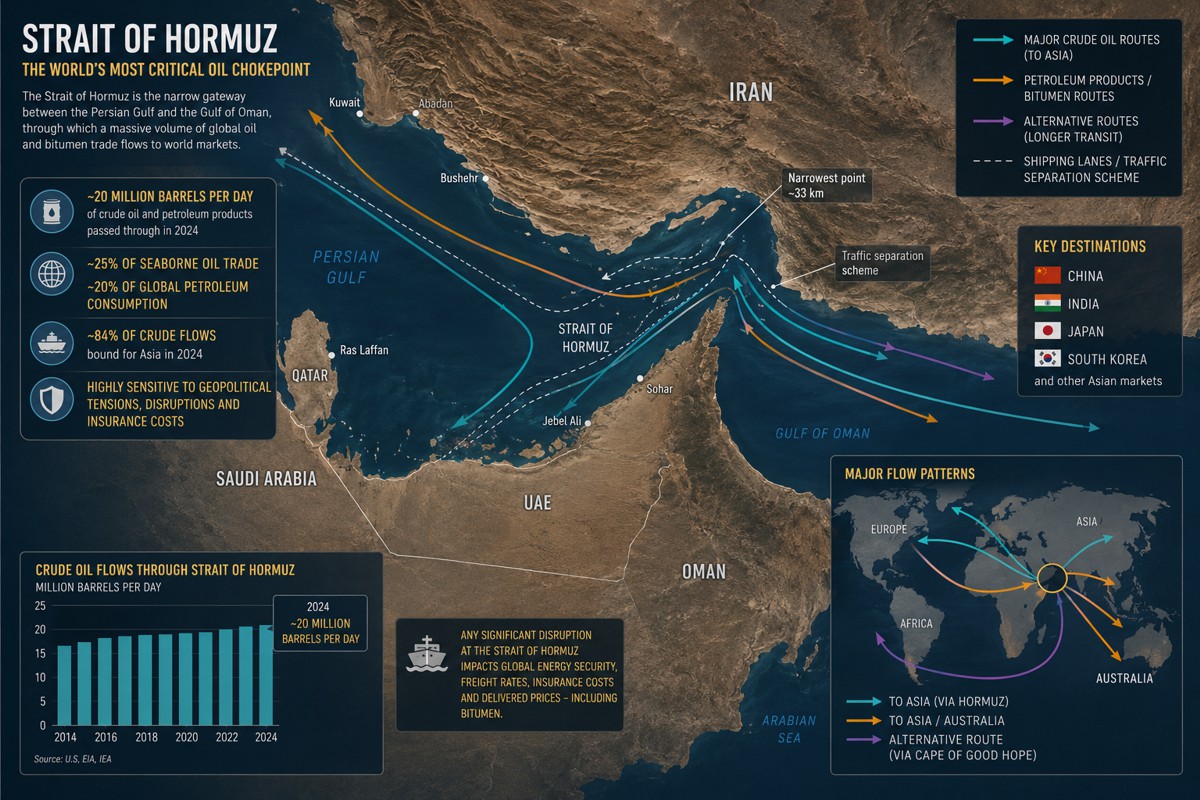

- The Strait of Hormuz is the single most important pinch point, underpinning India’s import balance and much of East and Southern Africa’s supply.

- A tiny, ageing specialised tanker fleet and the drum-versus-bulk packaging split mean small distance changes carry outsized cost effects.

- Resilience in this market is corridor-based, not supplier-based, which puts a premium on alternative origins, freight clauses and storage buffers written into tenders from the outset.

Why Hormuz now writes the road budget

Hormuz has always been the heavyweight of oil chokepoints, and the numbers explain why nobody in the bitumen trade can afford to ignore it. Roughly 20 million barrels a day of crude and products passed through the strait in 2024, which the US Energy Information Administration and the International Energy Agency reckon was around a quarter of all seaborne oil trade and close to a fifth of global petroleum consumption. About 84 per cent of that crude was bound for Asia, with China, India, Japan and South Korea soaking up the bulk of it. Bitumen is a niche product floating inside that giant flow, and when the flow constricts, the niche pays the price for scarce ships and pricier insurance.

In 2026 the risk stopped being academic. According to the figures gathered in the underlying research, the IEA judged that global oil supply fell by 10.1 million barrels a day in March 2026, Reuters estimated that more than 13 million barrels a day were effectively stranded in the Gulf, and the EIA flagged Middle East VLCC tanker rates at their highest since at least 2005.

India sits closest to the fire. The country imported just over US$1.02bn of petroleum bitumen in 2024, overwhelmingly from Iraq, the United Arab Emirates, Iran and Oman, with those four supplying roughly 2.79mn tonnes between them. Iraq alone accounted for about 1.52mn tonnes and the UAE another 0.96mn. India isn’t wholly import-dependent, since Argus put total domestic consumption at 8.44mn tonnes against imports of 2.8mn tonnes in 2024, but it leans hard on Gulf marginal barrels to balance a relentless road-building cycle, which is exactly why it’s usually the first market where freight dislocation shows up in delivered prices.

How the bitumen map is really drawn

Step back from the crisis headlines and the structure of the global bitumen trade is concentrated without being monocentric. Canada led the export side in 2024 with US$2.27bn and 5.01mn tonnes, a North American anchor tethered tightly to American demand. Singapore came second on US$1.33bn and 2.78mn tonnes, proof of how much refining, blending and re-export muscle counts in Asia. Iraq ranked third at US$1.11bn and 3.03mn tonnes, confirming the Gulf’s growing pull into South Asia, while Greece and Turkey, on US$0.53bn and US$0.50bn respectively, held down the Mediterranean’s role as a swing basin.

On the buying side the United States was the giant at US$2.46bn and 5.63mn tonnes, trailed by China, India, Australia and Algeria, each plugged into a different supply geography.

What that really shows is a market that’s continental and maritime at the same time. The Canada-to-US lane is enormous, but the geopolitically twitchy corridors run elsewhere, from the Gulf into India and Africa, from Singapore into South-East Asia and Australia, and from the Mediterranean into the Maghreb and West Africa.

For a sense of scale, market researchers valued the global bitumen business at somewhere between US$56bn and US$77bn in 2023 depending on methodology, with road construction taking the lion’s share and Asia-Pacific accounting for close to a third of demand. Because bitumen cargoes tend to be smaller, warmer and fussier than mainstream fuel oil or crude parcels, the whole map can pivot quickly the moment one origin loses barrels or a route picks up a war-risk premium.

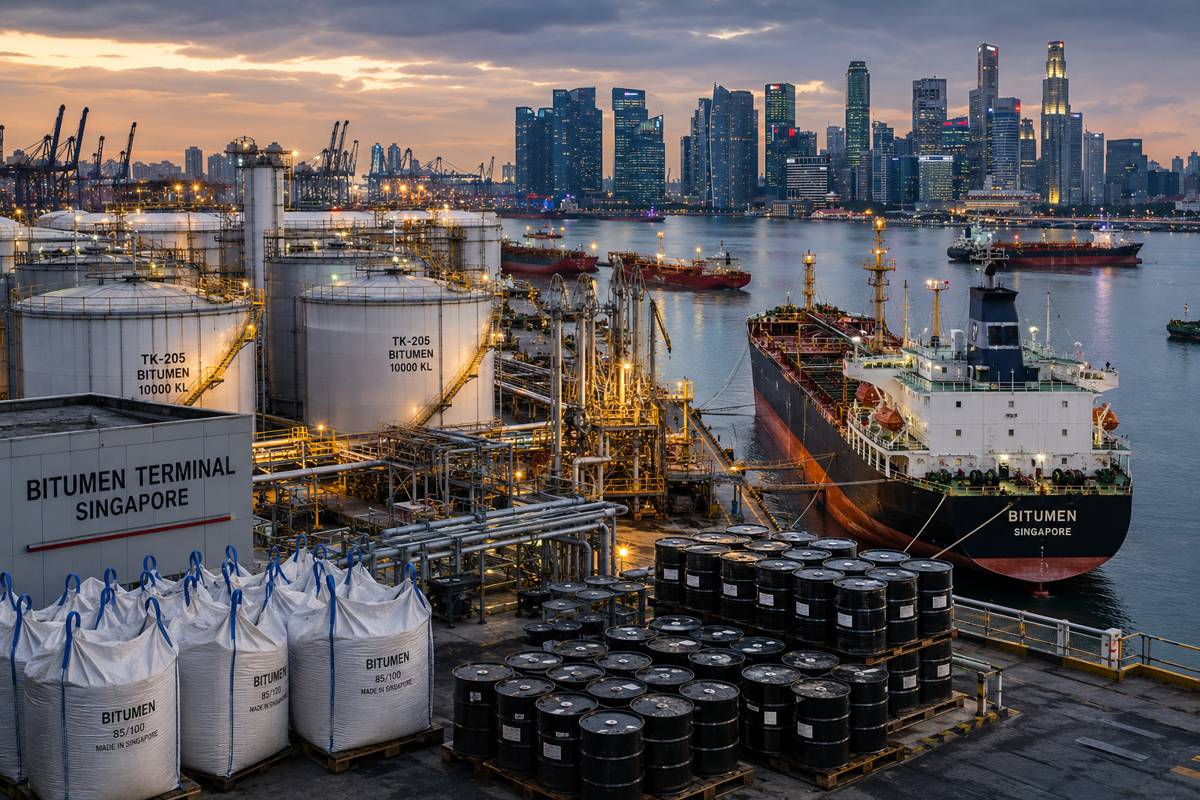

Singapore, Asia’s switching yard

Singapore’s place in the system is best read through a mismatch. The city-state exported US$1.33bn of bitumen in 2024 and ranked as the world’s second-largest seller, yet it imported a paltry US$8.76mn and 17,046 tonnes, mostly from Malaysia and South Korea. That tells you it isn’t a demand sink at all. It’s a conversion, blending, storage and redistribution hinge, and the destination data backs it up. In 2023 it pushed sizeable volumes into Indonesia, China, Malaysia, Vietnam and Australia, and in 2024 Indonesia alone leaned on Singapore for around 809,614 tonnes. Big hydrocarbon terminals, deep financing, price discovery and dense tanker connectivity hand traders an optionality that smaller regional suppliers simply can’t match.

The wider port story reinforces the point. Singapore logged record bunker sales of 54.92mn tonnes in 2024, ship arrivals of 3.11bn gross tonnes and container throughput of 41.12mn TEU, with analysts tying part of that uplift to Red Sea reroutings that funnelled extra traffic through the hub. Even Gulf players keep paying for the privilege; Reuters reported that ADNOC leased around 160,000 cubic metres of storage at Jurong Port Universal Terminal in early 2026, and while the lease was for fuel oil rather than bitumen, it signals where the optionality lives. The hub cuts both ways, though. When Argus reported in April 2026 that at least two major Singapore refiners declared force majeure on bitumen exports amid feedstock trouble, prices spiked to historic highs and importers in Indonesia and Australia had to reach further afield, into South Korea, Thailand or even the Middle East. A switching yard, it turns out, can transmit shocks as smoothly as it absorbs them. This exposes a broader truth: redundancy in bitumen supply increasingly depends on logistics hubs rather than producing nations.

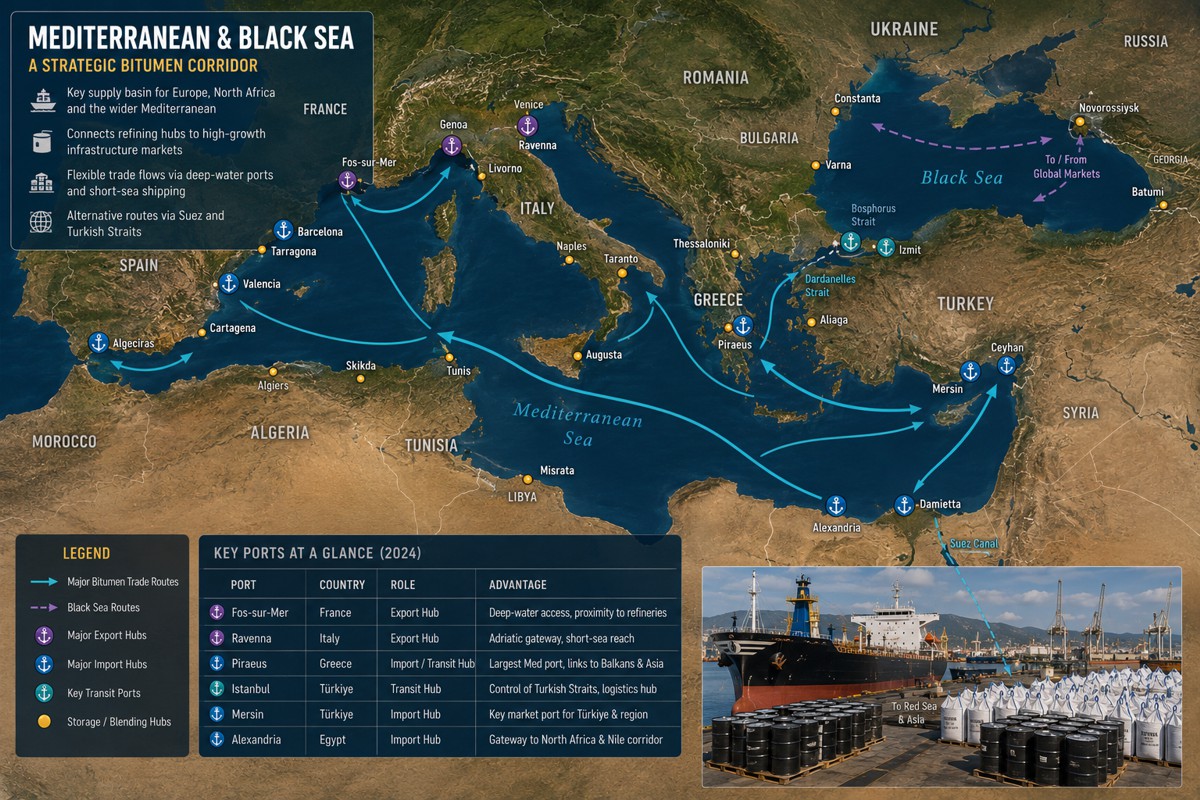

The Mediterranean swing and the Black Sea shadow

The Mediterranean is the trade’s most flexible and most politically revealing stretch. Greece shipped 1.20mn tonnes in 2024 to the likes of Romania, the United States, North Macedonia, Libya, Algeria and Morocco. Spain sent 721,633 tonnes, mostly to France, Morocco, Portugal, the UK and Cameroon. Italy moved 1.08mn tonnes with Algeria as its standout customer, and Turkey exported 1.17mn tonnes towards Togo, Romania, France, the UK and Ireland. Far from a closed basin, it’s a swing belt linking southern Europe to North and West Africa, the Balkans and parts of the Atlantic. And it reacts fast. Argus found North African buyers drifting away from Greek cargoes towards Spanish and Italian barrels in early 2026, with North African imports of Greek bitumen sliding to 65,000 tonnes in the first quarter from 164,000 a year earlier.

The Black Sea matters less for its own bitumen tonnage than for the energy traffic it shadows. Official Turkish data recorded 9,669 hazardous-cargo tankers carrying 167.3mn tonnes through the Bosporus in 2024, plus 10,450 tankers and 188.4mn tonnes through the Dardanelles, so any incident in the Straits ripples across the whole network that Mediterranean and Eastern European bitumen relies on.

Demand in that corner has also partly come off the water. Ukraine’s 2024 imports arrived chiefly by truck from Poland and Lithuania, and Argus put 2025 volumes at 190,000 tonnes, the highest since 2021. Romania makes the neatest case study of the overlap, importing about 734,095 tonnes in 2024 from Greece, Turkey and neighbours, while a new truck e-trading system threatened border congestion, a reminder that corridor resilience here hangs on customs admin as much as on ships.

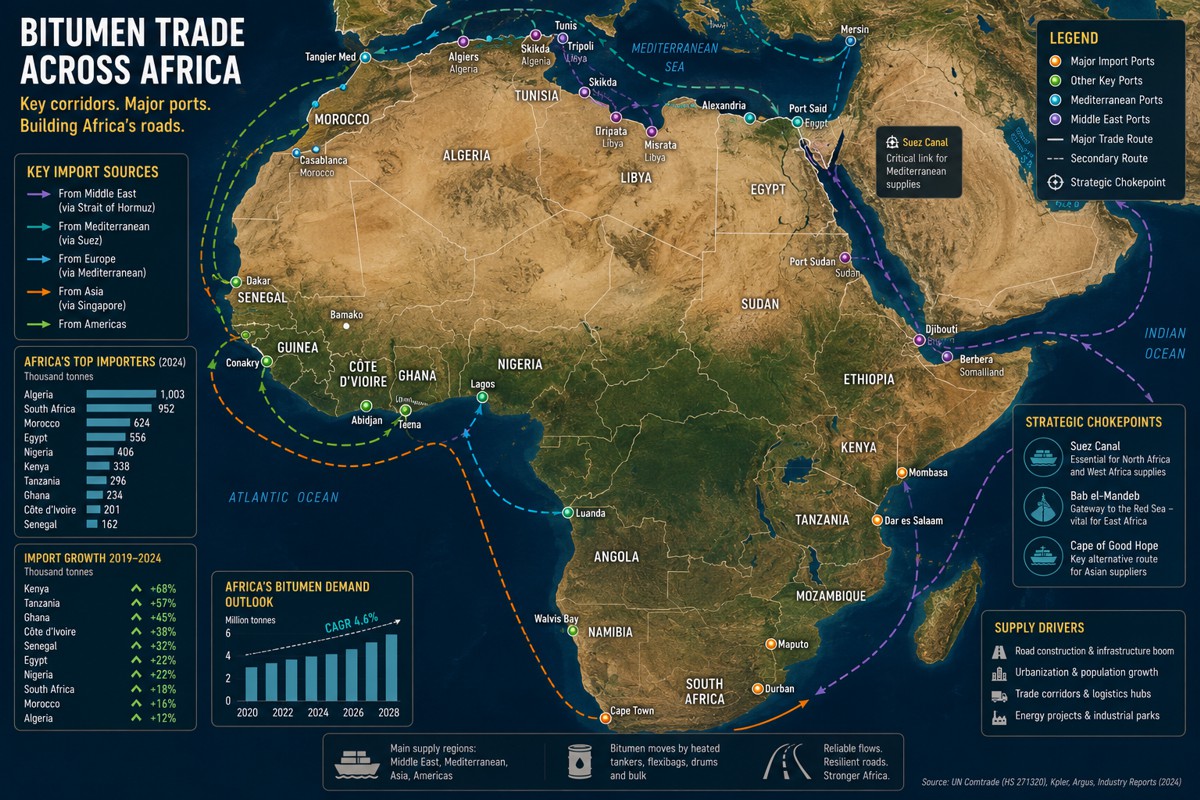

Africa’s freight squeeze

Africa’s reliance on imported bitumen is heavy, but it splits along clear lines. North Africa is wedded to the Mediterranean; Morocco took 471,319 tonnes in 2024 from Spain, Greece, Italy, Egypt and the Netherlands, and Algeria stood among the biggest importers by value, with Italy naming it the top destination for its exports. That ties Maghreb road budgets to western Mediterranean refinery output and to any freight wobble around Gibraltar or the central Med. West Africa runs on a blend of Mediterranean cargoes and regional redistribution, with Nigeria buying US$172.4mn worth in 2024 from Côte d’Ivoire, Türkiye, Greece, Spain and Pakistan, and Côte d’Ivoire itself exporting US$95mn, enough to make Abidjan a genuine regional platform rather than a pure end-market.

East and Southern Africa are the most Gulf-facing of all, and that’s where the 2026 freight squeeze bit hardest. South Africa’s import basket drew on Türkiye, Bahrain, Pakistan, Greece, Togo, the UAE, Iraq and Oman, while Kenya leaned on the UAE, Iran, Oman and Kuwait. The trouble is that in drummed or bagged markets, freight can swallow a huge chunk of landed cost in no time. Argus assessed direct container shipping to Mombasa and Dar es Salaam at roughly US$55 to US$70 a tonne in late February 2026, with drummed freight at US$90 to US$110. By April, with Iran-war surcharges in play, drummed freight from Bandar Abbas or Jebel Ali to Mombasa, Dar es Salaam and Djibouti had jumped to around US$230 a tonne. When the cost of moving the stuff more than doubles in eight weeks, the headline bitumen price becomes a secondary number, and the contractor footing the bill knows it.

A small fleet doing heavy lifting

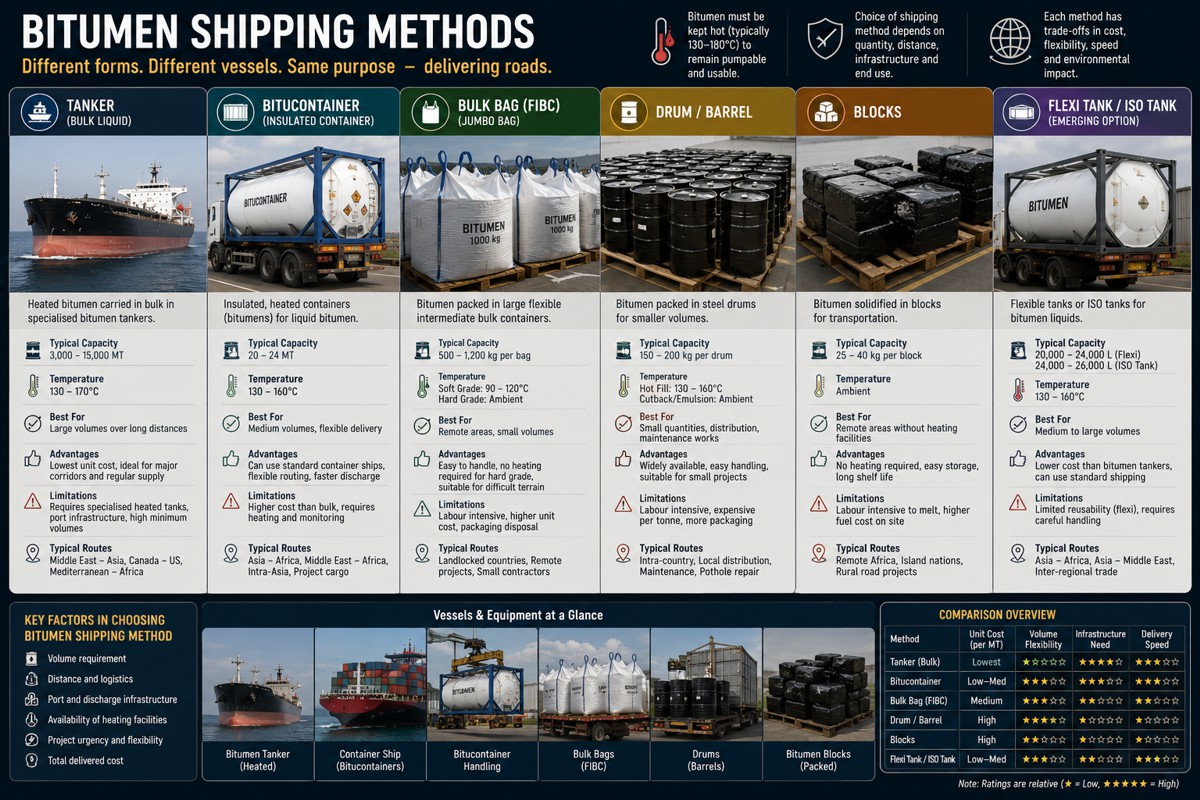

The physics of moving bitumen explain a lot of the cost behaviour. The cargo has to stay liquid, which means insulated, heated tanks and tight temperature control, typically in the 170 to 190 degree range, with some carriers built to handle up to about 250 degrees. The dedicated fleet that does this work is small and getting on a bit. Argus pegged it at roughly 230 vessels in 2024, averaging 15 years old and around 8,000 deadweight tonnes apiece. By global tanker standards that’s tiny, which is precisely why bulk bitumen freight rarely tracks the economics of big clean or dirty tankers, and why a handful of vessels going off-hire can tighten an entire region.

Where terminals lack heated bulk infrastructure, drums and containers fill the gap, and South African industry guidance notes that 20-foot bitumen boxes can even be heated in transit. The format lowers the entry threshold for smaller markets, but it turns brutal when container rates spike. The public freight references tell the same story from another angle. A short Gulf-to-India drummed run such as Bandar Abbas to Nhava Sheva sat at just US$19 to US$22 a tonne, while bulk on a comparable Bandar Abbas to Mundra route ran US$80 to US$90. Set those against broad dirty-tanker benchmarks of a few dollars a tonne for residual product, and it’s plain why bitumen prices the way it does. Distance, heat and scarcity stack up, and small differences in any one of them get amplified rather than averaged out.

Suez, the Bosporus and Panama

After Hormuz, the rest of the chokepoint map shapes vessel availability more than raw bitumen volume, but it shapes it forcefully. The Suez Canal and Bab el-Mandeb decide whether tankers stay on short Eurasian rotations or get bent around the Cape of Good Hope, burning more fuel and tying up tonnage. Red Sea attacks cut Bab el-Mandeb oil flows to 4.0mn barrels a day through August 2024, down from 8.7mn in 2023, and Suez Canal Authority data showed tanker transits falling from 8,435 in 2023 to 4,954 in 2024, with canal revenues sliding to about US$3.99bn from a record US$10.25bn. For bitumen buyers, that kind of disruption usually shows up in African and Mediterranean prices well before it lands in the customs figures.

The Turkish Straits and Panama play supporting roles, yet neither is trivial. The Bosporus is a systemic amplifier rather than a direct bitumen artery, so a weather closure or an incident there would jolt the wider energy network that Eastern European trades depend on. Panama, meanwhile, is more about vessel positioning than core volume, since most Latin American bitumen moves on Atlantic or coastal routes. Even so, the Panama Canal Authority logged 9,944 transits and 423.1mn tons in fiscal 2024, both dented by drought, before the EIA noted booking slots rising to 35 a day that August as water levels recovered. When one canal tightens, ships that might have repositioned between basins simply don’t, and freight stress in one corner of the oil world bleeds quietly into another.

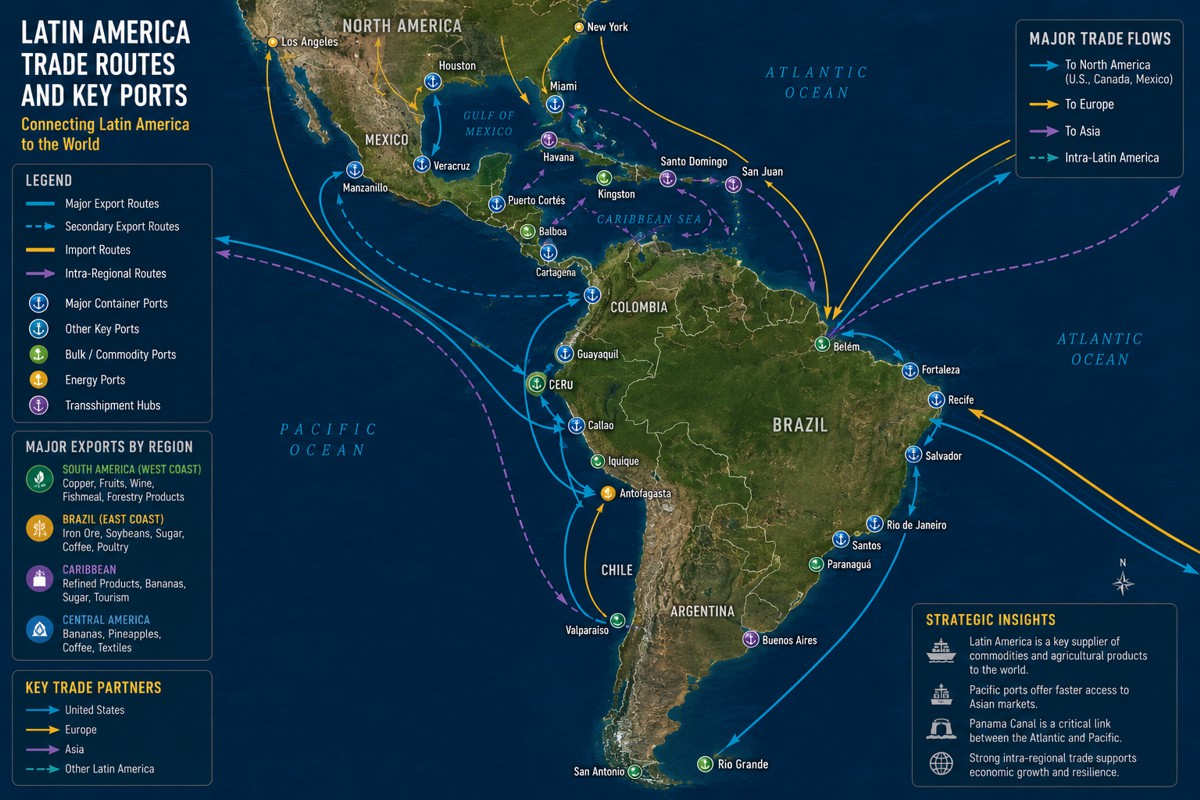

Latin America’s quieter web

Latin America is the least chokepoint-obsessed part of the picture, though it isn’t risk-free. The flows are hemispheric and fragmented rather than oceanic. Brazil imported 281,403 tonnes in 2024, mostly from the United States and Colombia, with side helpings from Kazakhstan, Russia and Italy. Uruguay took 112,481 tonnes, Argentina 76,266, and Mexico bought 162,178 tonnes entirely from the United States. Paraguay leaned mainly on Brazil. Read together, the lanes sketch three sub-systems: a US-anchored Atlantic and Gulf network feeding Mexico, Brazil and the Southern Cone; a Colombian and Brazilian regional web; and a small Central American cluster where Guatemala supplies El Salvador and Nicaragua.

That fragmentation cuts both ways for the people running the numbers. It shields the region from Hormuz, Suez and Bosporus drama far better than India or East Africa, but it ratchets up dependence on US Gulf Coast availability, Colombian export continuity and Atlantic freight conditions instead. Panama stays peripheral for most of these routes, which is largely good news, except when its drought-era slot cuts in 2023 and 2024 muddled vessel positioning across the basin. The takeaway for a regional contractor is that the danger isn’t a distant strait, it’s a hiccup at a single US refinery or a tightening of Atlantic freight, both of which can pinch supply with little warning.

Where this leaves the people who lay the roads

For road agencies, EPC contractors, importers and public works ministries, the recurring message is that resilience here is corridor-based, not supplier-based. A buyer who sources only from the cheapest Gulf origin isn’t diversified if every fallback still has to thread Hormuz. A North African buyer splitting volumes between Greece and Italy still shares common Mediterranean freight risk, but at least dodges plant-specific disruption. A West African buyer able to switch between Mediterranean cargo, Ivorian regional supply and Turkish exports holds real optionality. The practical fix is partly contractual, since delivered-price tenders ought to carry explicit freight, war-risk and delay clauses; the 2026 spikes proved that bitumen freight can reprice far quicker than annual road budgets, and FOB-only contracts just shove that volatility downstream onto the contractor.

The other half of the answer is physical and institutional. Markets that can take both bulk and containerised bitumen weather a crisis better than those locked into one discharge format, and the East African freight shock suggests that modest spending on storage, heating or inland decanting could pay for itself when project pipelines are large enough to justify bulk economics. Beyond the terminal gate, the smarter operators are building a compact monitoring dashboard covering Hormuz status and Gulf bypass capacity, Bab el-Mandeb and Suez transit trends, Turkish Straits traffic, Panama slot policy, Singapore export availability and sanctions-sensitive Russian and Iranian flows. None of that requires a trading desk. It just requires treating bitumen as a subset of transport security rather than a sack of cement that turns up on time, which, for countries with ambitious road plans and thin domestic refining, is now the difference between a project that runs to schedule and one that stalls at the first freight surprise.

For an industry measured in tonnes and kilometres, the next generation of road resilience may depend less on bitumen and asphalt and more on understanding the maritime routes that keep bitumen moving.