EBRD Backs Tavanbogd’s Hitachi Workshop in Mongolia

A MNT 143 billion loan for a maintenance shed is easy to underestimate. Read against where money and margin are actually moving in the heavy-equipment business, the European Bank for Reconstruction and Development’s latest Mongolian commitment looks less like real-estate finance and more like a wager on the service economy that keeps mining fleets running.

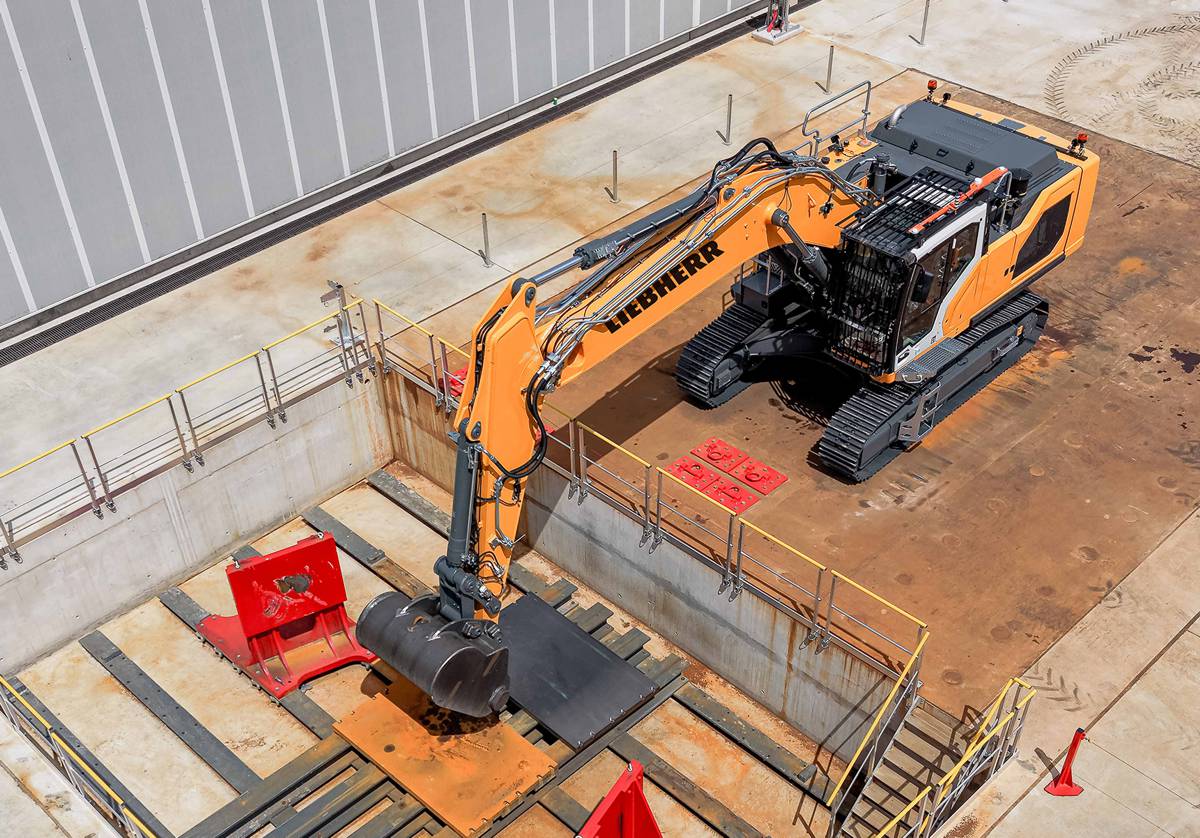

The Bank is lending up to MNT 143 billion, the equivalent of around €34.9 million, to Tavanbogd Construction Machinery, the official dealer for Hitachi heavy machinery in Mongolia and a client of the Bank since 2009. The headline use of funds is a modern maintenance workshop, a warehouse and office space, together with support for the dealer’s working capital.

The reason this matters beyond Ulaanbaatar is that the deal lands at the exact point where the global equipment industry is repricing its own value. Original equipment manufacturers no longer make their best returns on the day a machine leaves the yard. They make them across the decade that follows, through parts, servicing, remanufacturing, rebuilds and uptime guarantees.

For a market like Mongolia, where mining runs the economy and machines work in some of the harshest operating conditions on earth, the ability to service a fleet quickly and locally is not a convenience. It is the difference between a productive asset and an idle one, and increasingly it is where competitive advantage between the major manufacturers is decided.

Briefing

- The EBRD is providing a local-currency loan of up to MNT 143 billion (around €34.9 million) to Tavanbogd Construction Machinery, the official Hitachi heavy-machinery dealer in Mongolia and a Bank client since 2009.

- Funds will finance a modern maintenance workshop, a warehouse and office space, and will also support the dealer’s working capital requirements.

- The new facility will feature energy-efficient components including high-performance insulation, LED lighting, natural ventilation and heat pumps, backed by an incentive grant under the EBRD’s FINTECC climate-technology programme.

- The transaction fits Hitachi Construction Machinery’s strategic shift from volume manufacturing towards value-chain businesses such as parts, service, remanufacturing and rental, where a large and growing share of group revenue now sits.

- The EBRD has now invested more than US$3.2 billion (€2.8 billion) across 171 projects in Mongolia, with roughly 90 per cent directed at the private sector.

Where Value Is Migrating in Heavy Equipment

To understand why a dealer workshop attracts development-bank capital, it helps to look at what Hitachi Construction Machinery has been building since it parted company with John Deere. The dissolution of that long-standing Americas joint venture in 2022 forced the Japanese manufacturer to construct its own route to market rather than lean on a partner’s dealer network.

In the years since, it has pursued what the company itself describes as value-chain businesses, the activities beyond new-machine sales that cover parts and service, specialised mining aftermarket support, remanufactured components, rental and used equipment. Recurring aftermarket work now accounts for a substantial share of group revenue, reported in some assessments at around 40 per cent, and the manufacturer has explicitly reframed itself as a solutions provider rather than a maker of iron.

That repositioning exposes a genuine competitive gap. Analysts who compare Hitachi with Caterpillar and Komatsu tend to agree that its relative weakness is precisely the density and reach of its dealer-service ecosystem, the very asset that underpins Caterpillar’s durability. A purpose-built workshop, warehouse and parts operation in a mining economy is one of the clearest ways to close that gap, because it converts a manufacturer’s aftermarket ambition into physical capacity on the ground.

Seen in that light, the Tavanbogd investment is not a peripheral piece of dealer housekeeping. It is a local instalment of a global strategy, funded on terms that a commercial bank operating alone would be unlikely to match.

Mongolia’s Mining Fleet and the Uptime Imperative

Mongolia is an unusually pure test of the service-economy thesis because mining does so much of the heavy lifting in the wider economy. The sector accounts for close to a quarter of gross domestic product and the large majority of export earnings, anchored by the Oyu Tolgoi copper and gold complex in the South Gobi and by the coking-coal trade into China.

The underground expansion at Oyu Tolgoi has pushed copper output sharply higher, and record physical volumes of coal continued to move across the border even as prices softened through 2025. Each of those tonnes depends on excavators, haul trucks, loaders and drills that must keep working through Gobi dust and continental winters that few fleets anywhere endure.

The commercial subtlety is that a soft pricing cycle changes what operators want from their equipment, and it changes it in a way that favours exactly this kind of investment. When commodity prices fall, mine operators do not stop hauling; they haul harder to defend revenue on volume, and they scrutinise every cost that stands between them and a productive shift.

New-machine purchasing turns cyclical and cautious, a pattern visible in Mongolia’s recent import data, where machinery and vehicle-related imports have eased. Aftermarket demand behaves in the opposite direction. Fleets that are worked intensively and held longer generate more servicing, more parts consumption and a higher premium on rapid turnaround. A dealer that can rebuild a component in-country rather than shipping a machine out of service for weeks is selling the single thing a squeezed operator values most, which is time on the ground.

Local Currency and the FINTECC Green-Building Play

The structure of the loan carries as much significance as its purpose. By lending in Mongolian tögrög rather than hard currency, the EBRD removes the exchange-rate risk that would otherwise sit on the dealer’s balance sheet, a familiar hazard for import-dependent businesses whose costs are dollar-denominated but whose customers pay in local money.

The Bank has used the same logic in earlier Mongolian heavy-equipment transactions, and it matters more in a soft-price environment, when currency volatility can turn a manageable financing into a distressed one. Local-currency lending is one of the quieter ways development finance de-risks private investment, and it is often the feature that makes a long-dated capital project bankable at all.

The energy specification is the second lever. The new facility is designed around high-performance insulation, LED lighting, natural ventilation and heat pumps, a package aimed squarely at operating cost in a climate where heating dominates the annual energy bill. Ulaanbaatar is among the coldest capital cities in the world and carries a severe winter air-quality burden driven largely by coal combustion, which gives efficient, low-carbon building services a local resonance beyond the balance sheet.

The climate components are supported by an incentive grant under the EBRD’s Finance and Technology Transfer Centre for Climate Change, or FINTECC, which co-finances qualifying technologies as a complement to the Bank’s loan. FINTECC grants typically cover between 5 and 25 per cent of the cost of an eligible technology, are capped for early-transition countries such as Mongolia, and are paid only once the equipment is installed and commissioned. The design deliberately favours technologies with low market penetration, so that early adopters demonstrate their value and pull the wider market along behind them.

The Backbone Strategy Behind the Loan

This is not an isolated transaction, and its significance grows when placed in sequence. The EBRD and local lender Khan Bank supported another major heavy-equipment dealer, Wagner Asia Equipment, in 2020 through a risk-sharing facility that helped the distributor manage working capital through the pandemic. In 2024 the Bank financed a new energy-efficient automotive service centre for Tavan Bogd’s Toyota business, and in 2025 it extended further lending into the country’s automotive-service sector.

A pattern is visible across those deals, in which the Bank consistently targets the servicing, parts and maintenance layer of Mongolia’s vehicle and equipment economy rather than the machines themselves.

The rationale connects directly to the EBRD’s mandate in the country. The Bank has now committed more than US$3.2 billion across 171 projects in Mongolia, with roughly 90 per cent of that capital directed at the private sector, and in 2025 alone it invested US$218 million there, the bulk of it channelled through partner financial institutions.

Its stated priority is a stronger, more diversified and more resilient private economy, and equipment servicing fits that goal with unusual precision. It builds skilled technical employment, it deepens a domestic capability that would otherwise be imported, and it strengthens the reliability of the fleets on which the country’s dominant export sector depends. Financing the backbone of the equipment economy is a way of supporting mining productivity without taking direct commodity-price exposure, which is a prudent stance in a year when coal revenues have been under pressure.

What It Signals for Procurement and Competition

For mine operators and large contractors, the practical message is that dealer capability is becoming a procurement variable in its own right. The purchase decision on a hydraulic excavator or a rigid hauler increasingly turns on the parts-and-service infrastructure standing behind it, because lifecycle cost and guaranteed uptime now weigh as heavily as the sticker price.

A manufacturer that can promise a local rebuild, a stocked warehouse and a trained workshop within reach of the pit is offering a materially different total cost of ownership from one that cannot, and buyers in demanding environments are learning to price that difference accordingly. Investment that hardens a dealer’s service footprint therefore feeds straight into competitive position at the point of sale.

For the manufacturers, the deal illustrates how the contest between Hitachi, Caterpillar and Komatsu is playing out away from the showroom. Hitachi has been assembling the components of an aftermarket franchise, from its ownership of mining wear-parts and services specialists to autonomous haulage systems and dedicated regional structures in the Americas and Latin America.

Each localised workshop of the kind now being financed in Mongolia adds a node to that network and chips at the service-density advantage its larger rivals have long enjoyed. For international investors watching the sector, the signal is that recurring, higher-margin aftermarket revenue is where the equipment majors are concentrating effort, and that development finance is increasingly willing to underwrite the physical infrastructure that makes those revenues stick.

Reading the Signal

The most useful way to interpret this loan is as a small, precise indicator of a larger reallocation of value in the machinery business. The equipment itself is becoming, in commercial terms, the least differentiated part of the offer, while the service, parts and uptime wrapped around it become the arena where manufacturers win and lose.

Mongolia, with its mining-led economy, punishing operating environment and cyclical commodity revenues, compresses that logic into an especially clear case. A dealer that can keep the country’s fleets working, at a predictable cost, through a soft market and a hard winter, is holding something genuinely valuable.

That is why a maintenance workshop attracts a nine-figure commitment from a development bank, a currency structure built to survive volatility and a climate grant to hold down its running costs. The building is the visible object, but the asset being financed is capability, the capacity to service, sustain and extend the productive life of the machines on which Mongolia’s exports depend.

As the wider industry keeps shifting weight from selling iron to sustaining it, expect more capital to follow the same path, into the workshops, warehouses and parts operations that quietly determine whether the world’s heavy equipment is earning or standing still.

Key Industry Questions

- Why would a development bank finance a dealer’s maintenance workshop rather than the machinery itself? Because the servicing layer delivers more of the strategic outcomes a development bank targets. A workshop, warehouse and parts operation builds domestic technical skills, reduces reliance on imported repair capacity, and improves the reliability of fleets that underpin the country’s dominant export sector. It also supports private-sector productivity without taking direct exposure to commodity prices, which matters in a year of soft coal revenues. Financing the aftermarket backbone therefore advances economic diversification and resilience more effectively than funding machines that would be purchased in any case, while crowding in private capital on terms a commercial lender acting alone would rarely offer.

- How does the value chain shift in heavy equipment change purchasing decisions? Buyers increasingly evaluate the parts-and-service infrastructure behind a machine as carefully as its price and specification. In demanding environments, uptime and lifecycle cost dominate the economics, so a manufacturer able to guarantee local rebuilds, stocked parts and a trained workshop within reach of the site offers a materially lower total cost of ownership. That capability becomes a competitive lever at the point of sale. For fleet owners, the practical consequence is that dealer service density now belongs in the procurement scorecard alongside fuel burn, payload and residual value, rather than being treated as an afterthought once the purchase is made.

- What is the FINTECC programme and what does its grant actually do here? FINTECC is the EBRD’s Finance and Technology Transfer Centre for Climate Change, which provides incentive grants that complement the Bank’s loans when a project installs qualifying low-carbon technologies. The grants typically cover between 5 and 25 per cent of an eligible technology’s cost, are capped for early-transition countries such as Mongolia, and are paid only after the equipment is installed and commissioned. The mechanism deliberately favours technologies with low local market penetration, so early adopters demonstrate viability and help build a wider market. In this project it supports the insulation, LED lighting, ventilation and heat-pump systems that lower the facility’s long-term energy cost.

- Why lend in Mongolian tögrög rather than euros or dollars? Local-currency lending removes exchange-rate risk from the borrower’s balance sheet. Equipment dealers typically carry dollar-denominated costs while earning revenue in local currency, so a hard-currency loan would expose them to a mismatch that currency swings can turn dangerous, particularly during a soft commodity cycle. Lending in tögrög aligns the loan with the cash flows that service it, making a long-dated capital project more bankable and less fragile. It is one of the quieter but more consequential tools development finance uses to de-risk private investment, and the EBRD has applied the same approach in earlier Mongolian heavy-equipment transactions.

- Does weaker coal pricing undermine the case for investing in equipment servicing? The opposite tends to be true. When prices fall, operators haul harder to defend revenue on volume and scrutinise every cost between them and a productive shift. New-machine buying turns cautious, but existing fleets are worked more intensively and kept in service longer, which raises demand for parts, servicing and fast turnaround. A dealer able to rebuild components in-country rather than sending machines abroad for weeks is selling precisely what a cost-focused operator values most. Aftermarket demand therefore holds up, and can strengthen, in exactly the conditions that soften new-equipment sales, which makes servicing capacity a comparatively resilient investment.

- How does this deal fit Hitachi Construction Machinery’s wider strategy? Since dissolving its Americas joint venture with John Deere in 2022, Hitachi has built its own route to market and expanded what it calls value-chain businesses, spanning parts and service, mining aftermarket support, remanufacturing, rental and used equipment. Recurring aftermarket work now represents a large share of group revenue, and the manufacturer has recast itself as a solutions provider. Its relative weakness against Caterpillar and Komatsu is dealer-service density, so localised workshops and parts operations directly address that gap. A modern service facility in a mining economy such as Mongolia adds a node to that network and strengthens the aftermarket franchise the company is assembling globally.

- What does the transaction mean for Mongolia’s broader economic diversification? It deepens domestic industrial capability in a way that complements, rather than merely extends, the mining sector. Skilled maintenance, parts logistics and rebuild capacity create technical employment and retain value that would otherwise flow abroad with imported repair services. Because the capability supports the productivity of the export base without adding direct commodity exposure, it strengthens resilience against price cycles. It also fits the EBRD’s stated priority of a stronger, more diversified private economy, and sits within a consistent pattern of Bank investment in Mongolia’s vehicle and equipment servicing sector, from heavy machinery to the automotive market.

- Is there a wider signal here for investors in the equipment sector? Yes. The deal reflects a broader reallocation of value in the machinery industry, away from one-off machine sales towards recurring, higher-margin aftermarket revenue in parts, service and uptime. The equipment majors are concentrating strategic effort on that layer, and development finance is increasingly prepared to underwrite the physical infrastructure, the workshops, warehouses and parts networks, that makes those revenues durable. For investors, the readable trend is that service density and lifecycle capability are becoming the defensible assets in heavy equipment, and that capital is flowing towards the infrastructure that sustains machines rather than the machines themselves.

Strategic Takeaways

- The competitive frontier in heavy equipment has moved from the machine to the service around it, and localised parts, workshop and rebuild capacity is now a decisive factor in procurement, lifecycle cost and manufacturer market share.

- Aftermarket demand is counter-cyclical to new-equipment sales, so investment in servicing capability is comparatively resilient during soft commodity cycles when fleets are worked harder and held longer.

- Local-currency lending and climate-linked grants such as FINTECC are the structural tools that make long-dated private capital projects bankable in volatile, import-dependent markets, and their presence often signals development finance intent to de-risk rather than merely fund.

- The EBRD is systematically financing the servicing backbone of Mongolia’s equipment and vehicle economy, a strategy that supports mining productivity and private-sector diversification without taking direct commodity-price exposure.

- Hitachi Construction Machinery’s value-chain expansion, reinforced by facilities of this kind, is a deliberate move to close the dealer-service gap with Caterpillar and Komatsu, and investors should read continued capital flow into aftermarket infrastructure as the sector’s clearest strategic tell.